Key Points

Neoclassical economic theory assumes that economic actors are rational

Consumers are assumed to maximise their utility, workers their rewards from working, firms their profit

In neoclassical economic theory, economic actors make decisions at the margin

`Rational choice theory states that individuals use rational calculations to make rational choices and achieve outcomes that are aligned with their own personal objectives

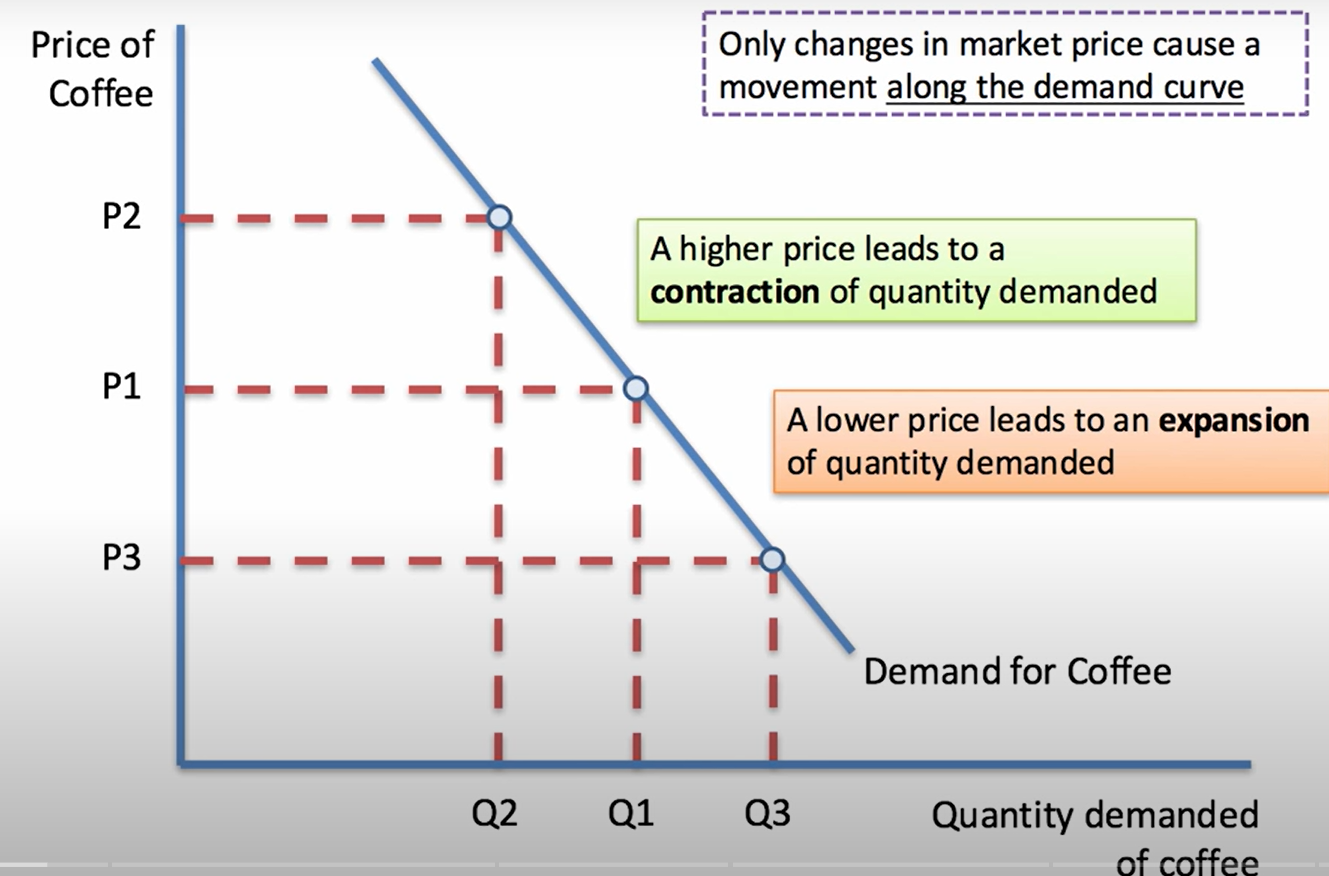

When building supply and demand models the assumption is made that consumers and producers act in a rational way to maximise their utility. The key aim of rational consumers is to maximise their own utility or satisfaction when making their choices. Often this might involve some cost-benefit calculation. - weighing up the benefits and costs of allocating some of their limited budget to different goods and services. Or deciding how much to save rather than spend in a given time period.

Consumer welfare refers to the outcomes for consumers from market activity. Consumer welfare can be illustrated using the concept of consumer surplus. Consumer surplus is highest at an equilibrium price where the price charged = the marginal cost of supply. However, firms with monopoly power can raise prices above a competitive level leading to a deadweight loss of consumer welfare. This means that there is a loss of allocative efficiency.

Self-Interest and the Invisible Hand

Adam Smith was one of the first economists to develop the underlying principles of the rational choice theory. Smith elaborated on his studies of self-interest and the invisible hand theory in his book “An Inquiry into the Nature and Causes of the Wealth of Nations,” which was published in 1776.

The invisible hand itself is a metaphor for the unseen forces that influence a free market economy. First and foremost, the invisible hand theory assumes self-interest. Both this theory and further developments in the rational choice theory refute any negative misconceptions associated with self-interest. Instead, these concepts suggest that rational actors acting with their own self-interest in mind can actually create benefits for the economy at large.

According to the invisible hand theory, individuals driven by self-interest and rationality will make decisions that lead to positive benefits for the whole economy. Through the freedom of production, as well as consumption, the best interests of society are fulfilled. The constant interplay of individual pressures on market supply and demand causes the natural movement of prices and the flow of trade. Economists who believe in the invisible hand theory lobby for less government intervention and more free-market exchange opportunities.

Similarly, the economist Richard Thaler pointed out further limitations of the assumption that humans operate as rational actors. Thaler's idea of mental accounting shows how people place greater value on some dollars than others, even though all dollars have the same value. They might drive to another store to save $10 on a $20 purchase but they would not drive to another store to save $10 on a $1,000 purchase.

{kind=link}