749504

Description

Flashcards by ntokozoyende, updated more than 1 year ago

|

|

Created by ntokozoyende

about 10 years ago

|

|

| Question | Answer |

| Markets | Physical places where goods and services are exchanged for money. (Included are online markets where products are sold using with the use of a credit card or money transfers) |

| Product Market | Where goods and services are bought and sold. |

| Factor market | Where factors of production such as labour are bought and sold. |

| Financial markets | 1. Foreign Exchange market (Forex): Where international currencies are traded, 2. Stock markets (eg. JSE, NSE etc): Where shares in companies are bought and sold. |

| Demand | The quantity of a good or service that consumers are willing and able to purchase at a given time period. |

| Law of demand | 1. Negative causal relationship between price and quantity demanded: "As the price of a product falls, the quantity demanded of the product usually increases, ceteris paribus" 2. |

| The relationship between an individual consumer's demand and market demand | Individual demand is the quantity that a consumer with purchase at a given price, ceteris paribus, whereas market demand is a sum of all the individual demand curves in the market. |

| The demand curve | The quantity of goods/services demanded increases as the price falls. |

| The demand curve | |

| Non-price determinants of demand (factors which change demand/ shift the curve) | 1. Income a. Normal goods (rise in income=rise in demand) eg. air travel b. Inferior goods (rise in income=fall in demand) eg. first price products 2. The price of other goods a. Substitutes fall in price of one product (chicken)=decrease in the demand of the other product (beef) b. Complements: Fall in the price of one of the products (DVDs)=increase in the demand for the other product (DVD players) c. Unrelated goods: Change in the price of one product will have no effect on the demand for the other product (cellphones and tea) 3. Tastes/ preferences: A change in taste in favour of a product will lead to a greater demand at every price. eg. advertising campaigns. 4. Other factors: a. Population size: Population growth=increased demand b. changes in population age structure: eg. more older people=greater demand for nursing homes c. changes in income distribution: eg. relatively poor are better off and the rich are worse off= increase in demand for basic necessities such as meat d. government policies changes: eg. ban of smoking=fall in demand e. seasonal changes eg. Increased demand warm coats and decreased demand for swimsuits in winter. |

| Movement along the demand curve |

Image:

economics8.gif (image/gif)

|

| Reasons for movement along the demand curve | 1. Change in price of the good 2. Income effect: When the price of the good falls, people will have more to spend (real income) 3. Substitution effect: when the price of the product falls, it will be relatively more attractive to people than other products whose prices have not changed. |

| Shift of the demand curve |

Image:

economics10.gif (image/gif)

|

| Reasons for shift of the demand curve | Non-price determinants of demand. |

| Movement along the curve vs. shift of the curve | |

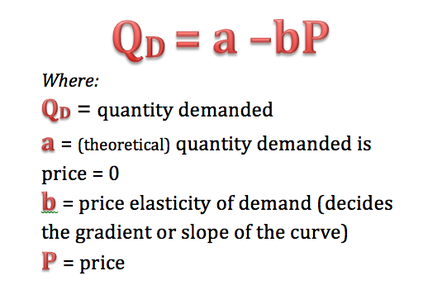

| The demand function (equation) | |

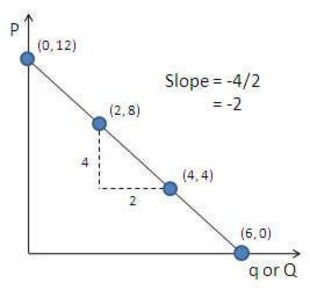

| Demand curve from linear equation |

Image:

demand_curve.gif (image/gif)

|

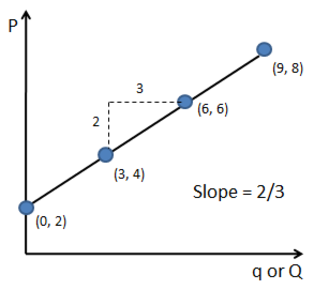

| Slope of the demand curve as the slope of the demand function. (-b is the coefficient of P) | |

| Why does changes in 'a' lead to a shift of the demand curve? | 'a' is the quantity demanded if the price were zero, the changes in 'a' refer to non-price determinants of demand and therefore will lead to the shift of the demand curve. |

| Why does a change in 'b' affect the steepness of the demand curve? | 'b' sets the slope of the curve as it is the coefficient of price. The curve becomes steeper for higher values of 'b' and the opposite is true. |

| Supply | The willingness and ability of producers to produce a quantity of a good or service at a given price in a given time period. |

| Law of supply | Positive causal relationship between price and quantity supplied: "as the price of a product rises, the quantity supplied of a product will usually increase, ceteris paribus. |

| The relationship between an individual producer supply and market supply | Individual producer supply is the quantity a producer is willing and able to supply at a given price whereas market supply is the sum of all individual producers' supply |

| The supply curve | The quantity of goods and services supplied increases as price increases. (upward facing curve) |

| The supply curve |

Image:

figure2.gif (image/gif)

|

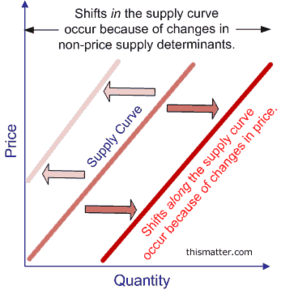

| Shift of the supply curve |

Image:

supplyshift.gif (image/gif)

|

| Reasons for shift of the supply curve | Non-price determinants of supply |

| Non-price determinants of supply | 1. Cost of factors of production: Increase in cost=higher supply costs =less supply 2. Price of related goods (joint/competitive supply): Produce skateboards vs. roller skates, choose the one with a greater demand=producers attracted to the one with the higher price= more supply 3. State of technology: Improvements in technology=increase in supply 4. Expectations: Future predictions for increased demand=assume higher prices=supply increased to meet demand at higher prices. 5. Government intervention: Indirect taxes=less supplied at each price whereas subsidies=more supplied at each price. |

| Movement along the supply curve | |

| Reasons for movement along the supply curve | Change in price of the good or service (Higher prices=greater profits and therefore increased supply and the opposite is true) |

| Shift of the supply curve vs. movement along the supply curve | |

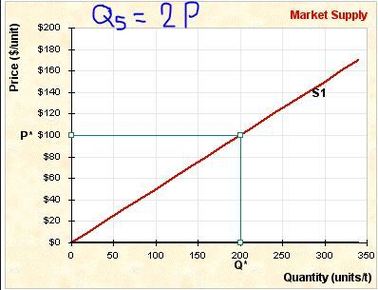

| The supply function(equation) | Qs= c + dP Qs: Quantity supplied c: Quantity supplied when price=0 d: Price elasticity of supply (gradient/slope) P: Price |

| Supply curve from linear eqaution | |

| slope of the supply curve as a slope of the supply function (d is the coefficient of P) |

Image:

Supply-Curve-4 (image/png)

|

| Why does 'c' lead to a shift of the supply curve? | 'c' is the quantity supplied of products when the price is equal to zero, the changes in 'c' refer to the changes in the non-price determinant of supply and therefore result in the shift of the supply curve. |

| Why does 'd' affect the steepness of the curve? (slope) | 'd' sets the slope of the curve as it is the coefficient of price. The curve becomes steeper for lower values of 'b' and the opposite is true. |

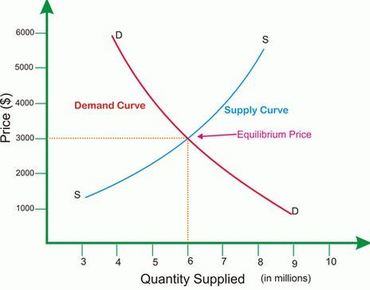

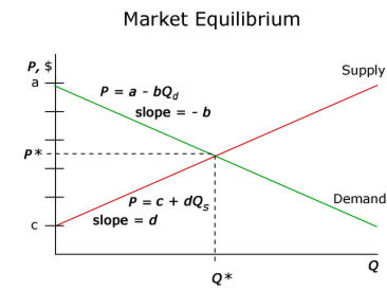

| Market equilibrium | The point when a good/ service are demanded and supplied for the same price. (The price and quantity is agreed upon by both the consumers and producers) |

| Market equilibrium |

Image:

market.JPG (image/JPG)

|

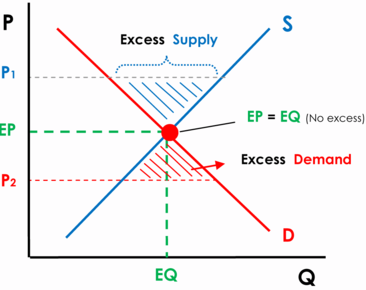

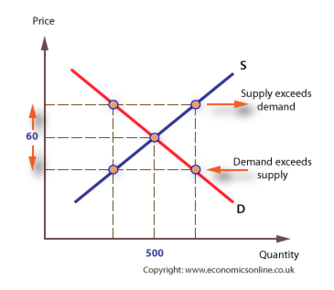

| Excess demand and supply | |

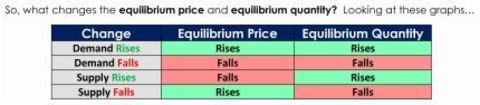

| Changes in demand and supply affecting equilibrium | |

| Changes in equilibrium price and quantity following changes in demand and supply |

Image:

effects.JPG (image/JPG)

|

| Equilibrium price and quantity equation (Qd=Qs) |

Image:

equilibrium.gif (image/gif)

|

| Demand and supply equations forming equilibrium (point of intersection) | |

| Excess supply: Qd<Qs Excess demand: Qs<Qd |

Image:

Excess-D-and-S (image/png)

|

| Price mechanism | How forces demand and supply move markets towards equilibrium. |

| Why does scarcity necessitate choices? | Infinite wants and finite resources require a trade off and therefore initiate the process of making choices. |

| Why does choice result in an opportunity cost? | Choice results in an opportunity as choosing one good over another requires one to forgo the potential of attaining the other good. |

| How is price a signalling and incentive function? (Invisible hand-Adam Smith) | 1. Resources are allocated and re-allocated in response to price changes. 2. An increase in the price of a good due to the increase in the demand for that good 'signals' to producers that consumers wish to buy this product. 3. Assuming that producers wish to maximise their profits, a higher price will give producers an incentive to produce more of a good. 4. No central planning agency: Price=signal and incentive |

| Consumer surplus | The extra satisfaction (utility) gained by consumers from paying a price lower than they were prepared to for a good/ service. |

| Consumer surplus(graphed) |

Image:

1431846_orig.gif (image/gif)

|

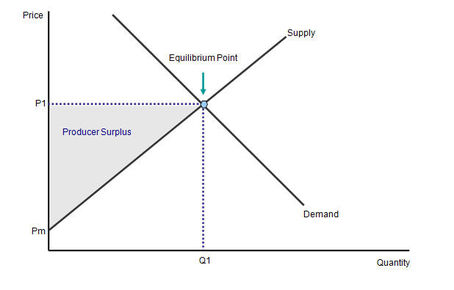

| Producer surplus | The excess of actual earnings a producer makes from a given quantity of output, over and above the amount the producer would be prepared to accept for that output. |

| Producer surplus (graph) | |

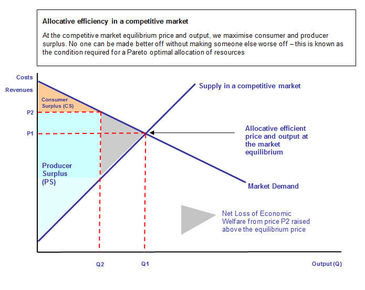

| Community surplus | The sum of consumer and producer surplus. This is also known as the total benefit to society. |

| Allocative efficiency from society's point of view | At equilibrium, where demand is equal to supply, consumer surplus is maximised. This is known as allocative efficiency. Given these conditions of demand and supply, there is no other combination of price and quantity that would give a greater community surplus. |

| Allocative efficiency (illustrated) |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.