1741583

Description

Mind Map by wanfarishaamirah, updated more than 1 year ago

|

|

Created by wanfarishaamirah

over 9 years ago

|

|

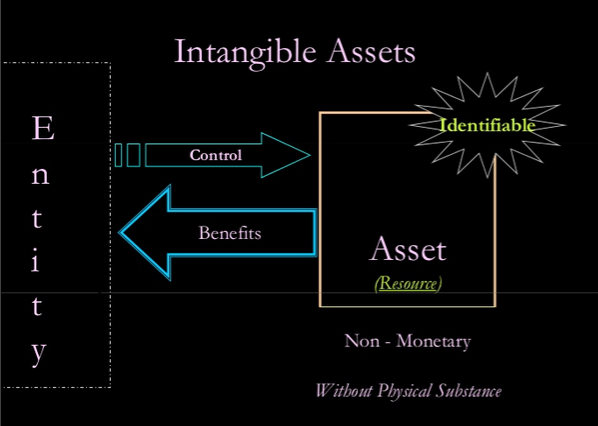

IAS 38 : INTANGIBLE ASSET

- DEFINITION

- Identifiable

- separable

- ↑ from :

contractual /

legal rights

- separable

- Non-monetary

- $ held

- A to be received in

DETERMINABLE amount

- $ held

- Asset

- control & past

event

- Control acieved

if entitiy has :

- ability-restrict access

- power- obtain f.e.b

- from legal rights ie copyright

- NOT NECESSARY but, more

DIFFICULT to PROVE if dont have it

- NOT NECESSARY but, more

DIFFICULT to PROVE if dont have it

- market & tech. knowledge

- from legal rights ie copyright

- power- obtain f.e.b

- ability-restrict access

- Control acieved

if entitiy has :

- expected f.e.b

- control & past

event

- w/o physical

substance

- Judgement: which is more significant

- Physical(tangible)

- IAS 16:PPE

- IAS 16:PPE

- Non-physical (intangible)

- IAS 38: IA

- IAS 38: IA

- Physical(tangible)

- Judgement: which is more significant

- Identifiable

- RECOGNITION

- Probable f.e.b flow

- assumed to be

satisfied in both

situation

- Reliably measured

- Cost measured @ FV

- FV= Market expectation of expected f.e.b

- FV= Market expectation of expected f.e.b

- IA separately identified

- sufficient information

- sufficient information

- Reliably measured

- assumed to be

satisfied in both

situation

- Reliably measured

- Probable f.e.b flow

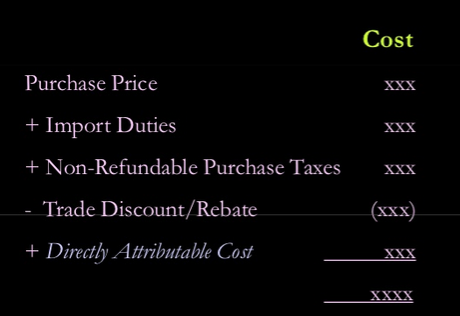

- MEASUREMENT

- INITIALly measured @ COST

- ACQUIRED

- Part of biz comb.

- FV @ acquisiton date

(FV= market expectation

of expected f.e.b)

- MP in ACTIVE MARKET

- MP in ACTIVE MARKET

- FV @ acquisiton date

(FV= market expectation

of expected f.e.b)

- Separately

- Part of biz comb.

- ACQUIRED

- SUBSEQUENT recognition

- Rev. needs

ACTIVE

MARKET

hence, X for:

- -brands

- mastheads

- patents/trademarks

- customers lists

- publishing titles

- publishing titles

- customers lists

- patents/trademarks

- mastheads

- -brands

- Rev. needs

ACTIVE

MARKET

hence, X for:

- INITIALly measured @ COST

- CAPITALISED

- purchased goodwill

- purchased IA

- DEVELOPMENT costs

- DEVELOPMENT costs

- purchased IA

- purchased goodwill

- EXPENSED

- start up cost

- training

- advert

- if paid, becomes asset : prepaid __

- if paid, becomes asset : prepaid __

- advert

- internally generated

- goodwill

- brand

- customer list

- training

- mastheads and publishing titles

- SUBSEQUENT EXP.

- due to nature of IA, usually cant be distinguished from cost of

developing biz as a WHOLE

- ALWAYS EXPENSED

- ALWAYS EXPENSED

- due to nature of IA, usually cant be distinguished from cost of

developing biz as a WHOLE

- SUBSEQUENT EXP.

- mastheads and publishing titles

- training

- customer list

- brand

- RESEARCH costs

- goodwill

- training

- UNLESS:

- forms part of the cost

- meets all recognition criteria

- meets all recognition criteria

- forms part of goodwill on BIZ COMB.

- forms part of the cost

- once

expensed

cannot be

capitalise

later on

- start up cost

- INTERNALLY GENERATED IA

- X meet definition and recognition criteria

- INTERNALLY GENERATED GOODWILL

- EXPENSED

- WHY?

- D

- X identifiable

- X control

- ✓ generate f.e.b

- ✓ generate f.e.b

- X control

- X identifiable

- R

- X measured realiably

- ✓ probable f.e.b

- ✓ probable f.e.b

- X measured realiably

- D

- WHY?

- EXPENSED

- INTERNALLY GENERATED GOODWILL

- ✓ meet definiiton and recognition criteria

- INTERNALLY GENERATED IA OTHER

THAN GOODWILL

- DIFFICULT to asses R criteria

- HENCE, additional requirement to classify asset generation into:

- RESEARCH phase

- DEFINITION

- original+planned investigation to gain new

scientific knowledge+understanding

- UNCERTAIN f.e.b will flow

(because it is merely and

investigation)

- UNCERTAIN f.e.b will flow

(because it is merely and

investigation)

- EXPENSE | ASSET

- EXAMPLES:

- activities - new knowledge

- search+evaluate - research findings

- search - alt new&improved materials, products, process (MPP)

- formulate+design+evaluate - alt MPP

- formulate+design+evaluate - alt MPP

- search - alt new&improved materials, products, process (MPP)

- search+evaluate - research findings

- Design+Construction+Testing - prototypes

- D tools involving new tech

- D+C+ operate - pilot plant

- D+C+T - new&improved MPP

- D+C+T - new&improved MPP

- D+C+ operate - pilot plant

- D tools involving new tech

- activities - new knowledge

- Recognised as ASSET if 6 criteria are met:

- G- generate feb

- A - ability to use

- M - measured reliably

- A - availability of resouce to complete

- T - technical feasibility

- I - intention to complete

- IF ONE OR MORE NOT MET - EXPENSED !

- IF ONE OR MORE NOT MET - EXPENSED !

- I - intention to complete

- T - technical feasibility

- A - availability of resouce to complete

- M - measured reliably

- A - ability to use

- recognised as asset meaning it

meets the 2 asset recognition

criteria- probable, reliably

- G- generate feb

- EXAMPLES:

- original+planned investigation to gain new

scientific knowledge+understanding

- DEFINITION

- DEVELOPMENT phase

- DEFINITION

- application of research findings

-- plan production of

new&improved items

- MORE ADVANCED stage of creation

- PROBABLE f.e.b flow

- PROBABLE f.e.b flow

- MORE ADVANCED stage of creation

- application of research findings

-- plan production of

new&improved items

- DEFINITION

- RESEARCH phase

- HENCE, additional requirement to classify asset generation into:

- DIFFICULT to asses R criteria

- INTERNALLY GENERATED IA OTHER

THAN GOODWILL

- eg: exp on brands, trademarks, customer

loyalty programme

- X meet definition and recognition criteria

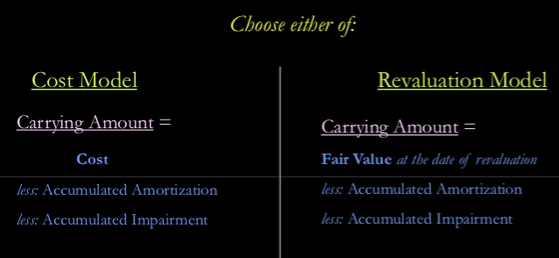

- USEFUL LIFE

- FINITE

- INDEFINITE

- X ammortised

- Test for impairment

- annually

- there is signs IA may be

IMPAIRED

- Useful life - reviewed each

period : determine if

indefinite life appropriate

(IF NOT change acc to IAS 8)

- annually

- Test for impairment

- X ammortised

- ✓ ammortised

- Residual value = 0 , unless :

- active market

- commitment by 3rd party to PURCHASE

- Amm. period+method: REVIEWED ANNUALLY

( acc to IAS 8)

- active market

- Residual value = 0 , unless :

- INDEFINITE

- FINITE

- RETIREMENT & DISPOSALS

- Derecognised when :

- disposal

- NO expected feb

- FORMULA: gain/loss = net proceed on disposal - CA ( cost/rev model)

- disposal

- Derecognised when :

Media attachments

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.