3037935

Description

Mind Map by Finian O'Driscoll, updated more than 1 year ago

More

|

|

Created by gjethwani

almost 9 years ago

|

|

|

|

Copied by Finian O'Driscoll

almost 9 years ago

|

|

Fundamental Economic Concepts

- Economic

Systems

- Market System

Annotations:

- Pure market systems are free of government intervention. Price mechanism is how the three questions are answered which makes the consumer soveriegn. Price acts as a signal, rationing device and incentive and can transfer preference. Firms respond to increased demands to achieve profits. The invisible hand. Assumption is consumers aim to maximise utility

- Centrally Planned

Annotations:

- 100% government influence and the 3 questions are attempted to be answered by them. Failed experiments in Soviet Union and China - Communists. No consumer or producer soveriegnity. Government decides what, how and for whom the produce goes to. Profit is not an objective. Factories get production targets.

- Mixed Economy

Annotations:

- Blend of market and planned economies. Quantity varies massively. Most ecnonomies are mixed. Most efficient as benefits of both government intervention and market forces.

- Market System

- Scarcity of Resources

- Opportunity Cost

- Next best alternative foregone

when a choice is made

- The Production

Possibility Frontier

(PPF)

Annotations:

- A curve depicting all maximum output possibilities for two or more goods given a set of inputs (resources, labor, etc.). The PPF assumes that all inputs are used efficiently.

- The Production

Possibility Frontier

(PPF)

- Next best alternative foregone

when a choice is made

- Infinite Needs but

Finite Resources

- Opportunity Cost

- Three Key Economic Questions

- What to produce?

- How to produce?

- For whom are the goods produced?

- What to produce?

- Theory of Comparative Advantage

Annotations:

- If our country can produce some set of goods at lower cost than a foreign country, and if the foreign country can produce some other set of goods at a lower cost than we can produce them, then clearly it would be best for us to trade our relatively cheaper goods for their relatively cheaper goods. In this way both countries may gain from trade.

- The theory of comparative advantage states that if countries specialise in producing goods where they have a lower opportunity cost – then there will be an increase in economic welfare.

- 4 Factors of Production

- Land

- Human Labour

- Capital & Investment

- Enterprise & Business

- Land

- Demand, Supply and

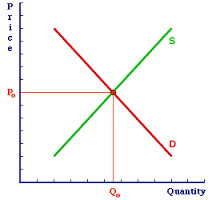

Market Equilibrium

Theory

- Law of Demand

- Law of Supply

- Equilibrium State/Price

- Economic Goods

- Price Elasticity

- Factors Affecting Demand & Supply

- Movements & Shifts in

Demand/Supply Behaviour

- Movements & Shifts in

Demand/Supply Behaviour

- Law of Demand

Media attachments

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.