13986541

Question 1

Question

Goodwill is

Answer

-

Seldom reported because it is too difficult to measure.

-

Reported when more than book value is paid in purchasing another company

-

Reported when the fair value of the acquiree is higher than the fair value of the net identifiable assets acquired

-

Generally smaller for small companies and increases in amount as the companies acquired increase in size

Question 2

Question

See image.

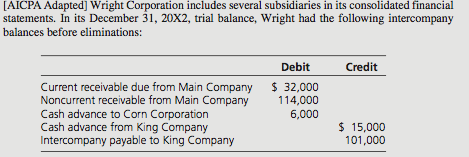

In its December 31, 20X2, consolidated balance sheet, what amount should Wright report as intercompany receivables?

{kind=link}

Answer

-

$152,000

-

$146,000

-

$36,000

-

$0

Question 3

Question

See Image.

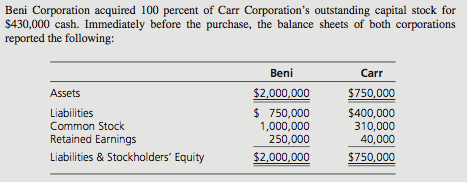

At the date of purchase, the fair value of Carr’s assets was $50,000 more than the aggregate carrying amounts. In the consolidated balance sheet prepared immediately after the purchase, the consolidated stockholders’ equity should amount to

{kind=link}

Answer

-

$1,680,000.

-

$1,650,000.

-

$1,600,000.

-

$1,250,000.

Question 4

Question

See Image.

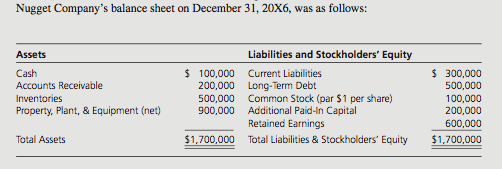

On December 31, 20X6, Gold Company acquired all of Nugget’s outstanding common stock for $1,500,000 cash. On that date, the fair (market) value of Nugget’s inventories was $450,000, and the fair value of Nugget’s property, plant, and equipment was $1,000,000. The fair values of all other assets and liabilities of Nugget were equal to their book values.

As a result of Gold’s acquisition of Nugget, the consolidated balance sheet of Gold and Nugget should reflect goodwill in the amount of

{kind=link}

Answer

-

$500,000

-

$550,000

-

$600,000

-

$650,000

Question 5

Question

On December 31, 20X6, Gold Company acquired all of Nugget’s outstanding common stock for $1,500,000 cash. On that date, the fair (market) value of Nugget’s inventories was $450,000, and the fair value of Nugget’s property, plant, and equipment was $1,000,000. The fair values of all other assets and liabilities of Nugget were equal to their book values.

Assuming Gold uses the equity method to account for investments and that Gold’s (unconsoli- dated) balance sheet on December 31, 20X6, reflected retained earnings of $2,000,000, what amount of retained earnings should be shown in the December 31, 20X6, consolidated balance sheet of Gold and its new subsidiary, Nugget?

Answer

-

$2,000,000

-

$2,600,000

-

$2,800,000

-

$3,150,000

Question 6

Question

On January 1, 20X1, Prim Inc. acquired all of Scrap Inc.’s outstanding common shares for cash equal to the stock’s book value. The carrying amounts of Scrap’s assets and liabilities approxi- mated their fair values, except that the carrying amount of its building was more than fair value. In preparing Prim’s 20X1 consolidated income statement, which of the following adjustments would be made?

Answer

-

Decrease depreciation expense and recognize goodwill amortization.

-

Increase depreciation expense and recognize goodwill amortization

-

Decrease depreciation expense and recognize no goodwill amortization

-

Increase depreciation expense and recognize no goodwill amortization

Question 7

Question

ThefirstexaminationofRuddCorporation’sfinancialstatementswasmadefortheyearended December 31, 20X8. The auditor found that Rudd had acquired another company on January 1, 20X8, and had recorded goodwill of $100,000 in connection with this acquisition. Although a friend of the auditor believes the goodwill will last no more than five years, Rudd’s manage- ment has found no impairment of goodwill during 20X8. In its 20X8 financial statements, Rudd should report

Answer

-

Amortization Expense: $0 Goodwill: $100,000

-

Amortization Expense: $100,000 Goodwill: $0

-

Amortization Expense: $20,000 Goodwill: $80,000

-

Amortization Expense: $0 Goodwill: $0

Question 8

Question

Consolidated financial statements are being prepared for a parent and its four subsidiaries that have intercompany loans of $100,000 and intercompany profits of $300,000. How much of these intercompany loans and profits should be eliminated?

Answer

-

Loans: $0 Profits: $0

-

Loans: $0 Profits: $300,000

-

Loans: $100,000 Profits: $0

-

Loans: $100,000 Profits: $300,000

Question 9

Question

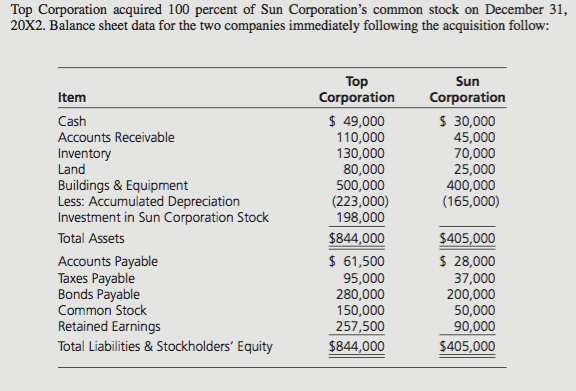

See Image.

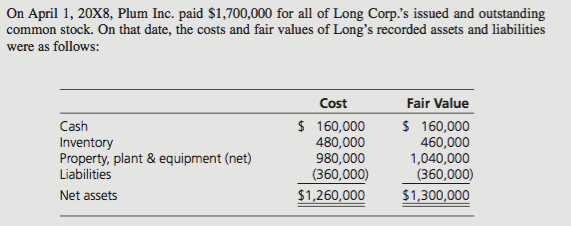

In Plum’s March 31, 20X9, consolidated balance sheet, what amount of goodwill should be reported as a result of this business combination?

{kind=link}

Answer

-

$360,000

-

$396,000

-

$400,000

-

$440,000

Question 10

Question

See Image.

At the date of the business combination, the book values of Sun’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000.

For each question, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of inventory will be reported?

{kind=link}

Answer

-

$70,000

-

$130,000

-

$200,000

-

$215,000

Question 11

Question

See Image.

At the date of the business combination, the book values of Sun’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000.

For each question, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of goodwill will be reported?

Answer

-

$0

-

$23,000

-

$43,000

-

$58,000

Question 12

Question

See Image.

At the date of the business combination, the book values of Sun’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000.

For each question, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of total assets will be reported?

Answer

-

$84,400

-

$1,051,000.

-

$1,109,000

-

$1,249,000

Question 13

Question

See Image.

At the date of the business combination, the book values of Sun’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000.

For each question, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of total liabilities will be reported?

Answer

-

$265,000.

-

$436,500

-

$701,500

-

$1,249,000.

Question 14

Question

See Image.

At the date of the business combination, the book values of Sun’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000.

For each question, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of consolidated retained earnings will be reported?

Answer

-

$547,500

-

$397,500

-

$347,500

-

$257,500

Question 15

Question

See Image.

At the date of the business combination, the book values of Sun’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000.

For each question, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of total stockholders’ equity will be reported?

Answer

-

$407,500

-

$547,500

-

$844,000

-

$1,249,000

Question 16

Question

If A Company acquires 80 percent of the stock of B Company on January 1, 20X2, immediately after the acquisition, which of the following is correct?

Answer

-

Consolidated retained earnings will be equal to the combined retained earnings of the two companies.

-

Goodwill will always be reported in the consolidated balance sheet.

-

A Company’s additional paid-in capital may be reduced to permit the carryforward of B Company retained earnings

-

Consolidated retained earnings and A Company retained earnings will be the same

Question 17

Question

Which of the following is correct?

Answer

-

The noncontrolling shareholders’ claim on the subsidiary’s net assets is based on the book value of the subsidiary’s net assets

-

Only the parent’s portion of the difference between book value and fair value of the subsid- iary’s assets is assigned to those assets

-

Goodwill represents the difference between the book value of the subsidiary’s net assets and the amount paid by the parent to buy ownership.

-

Total assets reported by the parent generally will be less than total assets reported on the consolidated balance sheet.

Question 18

Question

Which of the following statements is correct?

Answer

-

Foreign subsidiaries do not need to be consolidated if they are reported as a separate operating group under segment reporting

-

Consolidated retained earnings do not include the noncontrolling interest’s claim on the subsidiary’s retained earnings.

-

The noncontrolling shareholders’ claim should be adjusted for changes in the fair value of the subsidiary assets but should not include goodwill

-

Consolidation is expected any time the investor holds significant influence over the investee.

Question 19

Question

At December 31, 20X9, Grey Inc. owned 90 percent of Winn Corporation, a consolidated subsidiary, and 20 percent of Carr Corporation, an investee in which Grey cannot exercise significant influence. On the same date, Grey had receivables of $300,000 from Winn and $200,000 from Carr. In its December 31, 20X9, consolidated balance sheet, Grey should report accounts receivable from its affiliates of

Answer

-

$500,000

-

$340,000

-

$230,000

-

$200,000

Question 20

Question

A 70 percent owned subsidiary company declares and pays a cash dividend. What effect does

the dividend have on the retained earnings and noncontrolling interest balances in the parent company’s consolidated balance sheet?

Answer

-

No effect on either retained earnings or noncontrolling interest.

-

No effect on retained earnings and a decrease in noncontrolling interest.

-

Decreases in both retained earnings and noncontrolling interest.

-

A decrease in retained earnings and no effect on noncontrolling interest

Question 21

Question

How is the portion of consolidated earnings to be assigned to the noncontrolling interest in consolidated financial statements determined?

Answer

-

The parent’s net income is subtracted from the subsidiary’s net income to determine the noncontrolling interest

-

The subsidiary’s net income is extended to the noncontrolling interest

-

The amount of the subsidiary’s earnings recognized for consolidation purposes is multiplied by the noncontrolling interest’s percentage of ownership.

-

The amount of consolidated earnings on the consolidated worksheets is multiplied by the noncontrolling interest percentage on the balance sheet date

Question 22

Question

On January 1, 20X5, Post Company acquired an 80 percent investment in Stake Company. The acquisition cost was equal to Post’s equity in Stake’s net assets at that date. On January 1, 20X5, Post and Stake had retained earnings of $500,000 and $100,000, respectively. During 20X5, Post had net income of $200,000, which included its equity in Stake’s earnings, and declared dividends of $50,000; Stake had net income of $40,000 and declared dividends of $20,000. There were no other intercompany transactions between the parent and subsidiary. On December 31, 20X5, what should the consolidated retained earnings be?

Answer

-

$650,000.

-

$666,000.

-

$766,000.

-

$770,000.

Question 23

Question

On January 1, 20X8, Ritt Corporation acquired 80 percent of Shaw Corporation’s $10 par common stock for $956,000. On this date, the fair value of the noncontrolling interest was $239,000, and the carrying amount of Shaw’s net assets was $1,000,000. The fair values of Shaw’s identifiable assets and liabilities were the same as their carrying amounts except for plant assets (net) with a re- maining life of 20 years, which were $100,000 in excess of the carrying amount. For the year ended December 31, 20X8, Shaw had net income of $190,000 and paid cash dividends totaling $125,000.

In the January 1, 20X8, consolidated balance sheet, the amount of goodwill reported should be

Answer

-

$0

-

$76,000

-

$95,000

-

$156,000

Question 24

Question

On January 1, 20X8, Ritt Corporation acquired 80 percent of Shaw Corporation’s $10 par common stock for $956,000. On this date, the fair value of the noncontrolling interest was $239,000, and the carrying amount of Shaw’s net assets was $1,000,000. The fair values of Shaw’s identifiable assets and liabilities were the same as their carrying amounts except for plant assets (net) with a re- maining life of 20 years, which were $100,000 in excess of the carrying amount. For the year ended December 31, 20X8, Shaw had net income of $190,000 and paid cash dividends totaling $125,000.

In the December 31, 20X8, consolidated balance sheet, the amount of noncontrolling interest reported should be

Answer

-

$200,000

-

$239,000

-

$251,000

-

$252,000

Question 25

Question

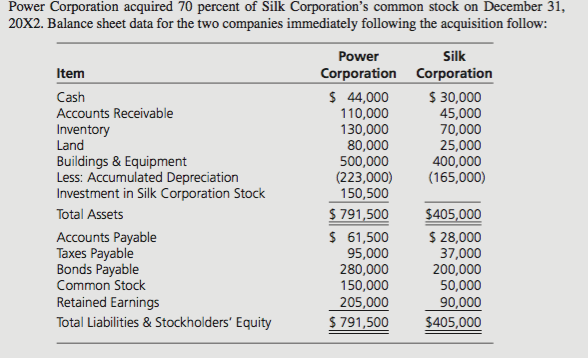

See Image.

At the date of the business combination, the book values of Silk’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000. The fair value of the noncontrolling interest was $64,500 on December 31, 20X2.

For each question below, indicate the appropriate total that should appear in the consolidated bal- ance sheet prepared immediately after the business combination.

What amount of inventory will be reported?

{kind=link}

Answer

-

$179,000

-

$200,000

-

$210,500

-

$215,000

Question 26

Question

See Image.

At the date of the business combination, the book values of Silk’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000. The fair value of the noncontrolling interest was $64,500 on December 31, 20X2.

For each question below, indicate the appropriate total that should appear in the consolidated bal- ance sheet prepared immediately after the business combination.

What amount of goodwill will be reported?

Answer

-

$0.

-

$28,000

-

$40,000

-

$52,000

Question 27

Question

See Image.

At the date of the business combination, the book values of Silk’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000. The fair value of the noncontrolling interest was $64,500 on December 31, 20X2.

For each question below, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of total assets will be reported?

Answer

-

$1,081,000

-

$1,121,000

-

$1,196,500

-

$1,231,500

Question 28

Question

See Image.

At the date of the business combination, the book values of Silk’s net assets and liabilities approxi- mated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000. The fair value of the noncontrolling interest was $64,500 on December 31, 20X2.

For each question below, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of total liabilities will be reported?

Answer

-

$265,000

-

$436,500

-

$622,000

-

$701,500

Question 29

Question

See Image.

At the date of the business combination, the book values of Silk’s net assets and liabilities approximated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000. The fair value of the noncontrolling interest was $64,500 on December 31, 20X2.

For each question below, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount will be reported as noncontrolling interest?

Answer

-

$42,000

-

$52,500

-

$60,900

-

$64,500

Question 30

Question

See Image.

At the date of the business combination, the book values of Silk’s net assets and liabilities approximated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000. The fair value of the noncontrolling interest was $64,500 on December 31, 20X2.

For each question below, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of consolidated retained earnings will be reported?

Answer

-

$295,000

-

$268,000

-

$232,000

-

$205,000

Question 31

Question

See Image.

At the date of the business combination, the book values of Silk’s net assets and liabilities approximated fair value except for inventory, which had a fair value of $85,000, and land, which had a fair value of $45,000. The fair value of the noncontrolling interest was $64,500 on December 31, 20X2.

For each question below, indicate the appropriate total that should appear in the consolidated balance sheet prepared immediately after the business combination.

What amount of total stockholders’ equity will be reported?

Answer

-

$355,000

-

$397,000

-

$419,500

-

$495,000

Question 32

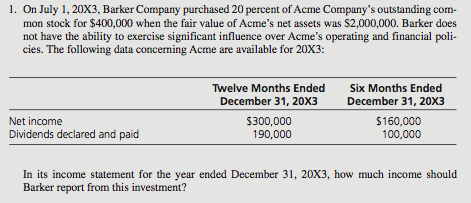

Question

See image.

In its income statement for the year ended December 31, 20X3, how much income should Barker report from this investment?

{kind=link}

Answer

-

$20,000.

-

$32,000.

-

$38,000.

-

$60,000.

Question 33

Question

OnJanuary1,20X3,MillerCompanypurchased25percentofWallCorporation’scommonstock; no differential resulted from the purchase. Miller appropriately uses the equity method for this investment, and the balance in Miller’s investment account was $190,000 on December 31, 20X3. Wall reported net income of $120,000 for the year ended December 31, 20X3, and paid dividends on its common stock totaling $48,000 during 20X3. How much did Miller pay for its 25 percent interest in Wall?

Answer

-

$172,000

-

$202,000

-

$208,000

-

$232,000

Question 34

Question

On January 1, 20X7, Robohn Company purchased for cash 40 percent of Lowell Company’s 300,000 shares of voting common stock for $1,800,000 when 40 percent of the underlying equity in Lowell’s net assets was $1,740,000. The payment in excess of underlying equity was assigned to amortizable assets with a remaining life of six years. As a result of this transaction, Robohn has the ability to exercise significant influence over Lowell’s operating and financial policies. Lowell’s net income for the year ended December 31, 20X7, was $600,000. During 20X7, Lowell paid $325,000 in dividends to its shareholders. The income reported by Robohn for its investment in Lowell should be

Answer

-

$120,000

-

$130,000

-

$230,000

-

$240,000

Question 35

Question

InJanuary20X0,FarleyCorporationacquired20percentofDavisCompany’soutstandingcom- mon stock for $800,000. This investment gave Farley the ability to exercise significant influence over Davis. The book value of the acquired shares was $600,000. The excess of cost over book value was attributed to an identifiable intangible asset, which was undervalued on Davis’ balance sheet and had a remaining economic life of 10 years. For the year ended December 31, 20X0, Davis reported net income of $180,000 and paid cash dividends of $40,000 on its common stock. What is the proper carrying value of Farley’s investment in Davis on December 31, 20X0?

Answer

-

$772,000

-

$780,000

-

$800,000

-

$808,000

Want to create your own Quizzes for free with GoConqr? Learn more.