3848266

Descripción

Test por Justin Guy (just, actualizado hace más de 1 año

|

|

Creado por Justin Guy (just

hace más de 8 años

|

|

Pregunta 1

Pregunta

A parent-subsidiary controlled group exists if the companies are connected through at least 50 percent stock ownership.

Respuesta

- True

- False

Pregunta 2

Pregunta

A brother-sister controlled group exists if either the common ownership or the effective control test is satisfied.

Respuesta

- True

- False

Pregunta 3

Pregunta

Attribution between spouses does not apply if the couple is childless.

Respuesta

- True

- False

Pregunta 4

Pregunta

Attribution from a parent to a minor child applies only if the parent owns more than 50 percent of the business.

Respuesta

- True

- False

Pregunta 5

Pregunta

Company A and Company B are a controlled group. The workforces of both companies are considered when testing each company’s plan for coverage requirements.

Respuesta

- True

- False

Pregunta 6

Pregunta

A financial institution is considered a service organization because it provides a service of lending money.

Respuesta

- True

- False

Pregunta 7

Pregunta

In order for an A-Org group to exist, the A-Organization must have at least a 10 percent ownership interest in the FSO.

Respuesta

- True

- False

Pregunta 8

Pregunta

If an FSO is a corporation, it always must be a professional service corporation for affiliated service group rules.

Respuesta

- True

- False

Pregunta 9

Pregunta

If two or more entities are deemed to be an affiliated service group, they do not need to be tested together for top-heavy purposes as long as each is not top-heavy on its own.

Respuesta

- True

- False

Pregunta 10

Pregunta

If two or more entities are deemed to be an affiliated service group and each entity sponsors its own plan, each plan must pass coverage.

Respuesta

- True

- False

Pregunta 11

Pregunta

For purposes of determining any type of affiliated service group, ownership is attributed from a grandchild to a grandparent, but not from a grandparent to a grandchild.

Respuesta

- True

- False

Pregunta 12

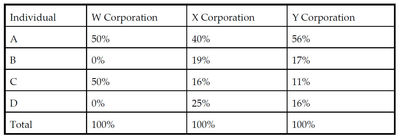

Pregunta

Based on the following information, determine brother-sister controlled group status:

• The individuals listed are not related.

{kind=link}

Respuesta

-

A. None

-

B. W and X only

-

C. W and Y only

-

D. X and Y only

-

E. W and X, X and Y only

Pregunta 13

Pregunta

All of the following conditions are necessary to avoid spousal attribution for controlled group purposes, EXCEPT:

Respuesta

-

A. The spouse must not have any direct ownership in the business.

-

B. The spouse must not be a director or employee of the business.

-

C. The spouse must not participate in the management of the business.

-

D. The spouse must not inherit the business upon death of the business owner.

-

E. No more than 50 percent of the business’ gross income may be derived from passive investments.

Pregunta 14

Pregunta

All of the following statements regarding attribution for controlled group purposes are TRUE, EXCEPT:

Respuesta

-

A. Ownership is attributed from husband to wife unless the business is wholly owned by the husband and certain requirements are met.

-

B. Ownership is attributed from a minor child to a parent.

-

C. Ownership is attributed from an adult child to a parent if the parent owns more than 50 percent of the corporation.

-

D. Ownership is attributed from a grandparent to a grandchild if the grandchild owns more than 50 percent of the corporation.

-

E. Ownership is attributed from a father-in-law to a son-in-law.

Pregunta 15

Pregunta

All of the following IRC sections consider controlled group members as a single employer, EXCEPT:

Respuesta

-

A. Eligibility and coverage (IRC §410)

-

B. Deduction (IRC §404)

-

C. Top-heavy (IRC §416)

-

D. Vesting (IRC §411)

-

E. Annual additions (IRC §415)

Pregunta 16

Pregunta

All of the following statements regarding affiliated service groups are TRUE, EXCEPT:

Respuesta

-

A. An FSO can be part of both an A-Org group and a B-Org group.

-

B. An FSO of an A-Org group must be a professional service organization.

-

C. An A-Organization must be a service organization.

-

D. A B-Organization need not be a service organization.

-

E. An A-Organization must have some ownership in the FSO.

Pregunta 17

Pregunta

All of the following are effects of being an affiliated service group, EXCEPT:

Respuesta

-

A. An employee’s service with all group members is credited when determining plan eligibility.

-

B. Plans must satisfy coverage requirements considering all employees in the affiliated service group.

-

C. HCE status is determined by looking at the ownership in each entity separately.

-

D. Annual additions for all plans in the group are aggregated to determine if the IRC §415 limits have been exceeded.

-

E. An employee’s service with all group members is credited when determining vesting percentages.

Pregunta 18

Pregunta

All of the following statements regarding attribution in determining affiliated service groups are TRUE, EXCEPT:

Respuesta

-

A. Ownership interest is attributed between spouses.

-

B. Ownership interest is attributed from parent to adult child only if the parent owns more than 50 percent of the company.

-

C. Ownership interest is not attributed between siblings.

-

D. Ownership interest is attributed from grandchild to grandparent.

-

E. Ownership interest is not attributed from grandparent to grandchild.

Pregunta 19

Pregunta

All of the following activities would be considered management functions, EXCEPT:

Respuesta

-

A. Supervisory roles

-

B. Hiring employees

-

C. Investing 401(k) plan assets

-

D. Setting employee compensation

-

E. Business planning

¿Quieres crear tus propios Tests gratis con GoConqr? Más información.