7236375

Description

Flashcards by Sophie Knight, updated more than 1 year ago

|

|

Created by Sophie Knight

about 9 years ago

|

|

| Question | Answer |

| Define monopolistic competition | "A market structure with many small firms that have differentiated products and low barriers to entry" |

| Give 4 examples of monopolistic competition | 1. Restaurants 2. Hotels 3. Pubs 4. Hairdressers |

| How efficient are firms in monopolistic competition? | They are neither productively or allocatively efficient |

| What happens in the long run firms operating in monopolistic competition? | They cannot maintain the supernormal profits because of the near perfect market knowledge and low barriers to entry so they are in long run equilibrium |

| What are the 5 characteristics of a monopoly? | 1) One firm (pure monopoly) 2) A unique product 3) Imperfect knowledge in the market 4) High barriers to entry and exit 5) Price maker |

| What are the 4 main disadvantages of a monopoly? | 1) Welfare loss 2) Loss of economic efficiency 3) Redistribution effect (consumers to shareholders) 4) Less consumer choice |

| What are the 4 main benefits of monopolies? | 1) Dynamic efficiency is possible because of supernormal profits being sustained in the long run 2) Global competition is possible 3) Economies of scale 4) Cross-subsidisation |

| What are the 2 costs to firms of being a monopoly? | 1) Inefficient (Productively, allocatively as well as X-inefficiency) 2) High start up costs |

| What are the 3 benefits to firms of being a monopoly? | 1) Supernormal profit in the long run due to being a price maker. 2) No competition threat 3) Can be dynamically efficient |

| What are the 4 costs to the consumer of a monopoly market? | 1) Little choice as there's no substitutes 2) Often higher prices, reducing consumer surplus 3) Less output than in a competitive market 4) Below social optimum |

| What are the 3 benefits to the consumer of a monopoly market? | 1) Cross-subsidisation provides products that may not have been previously 2) Could see lower prices due to economies of scale if producers pass them on 3) Dynamically efficient firms could invest into new and higher quality products |

| If a monopolist faces a decrease in demand, other things remaining equal, what will happen to price, profit and output? | Output will fall Price will fall Profit will fall |

| Define price discrimination | "Charging different prices to different groups of consumers for an identical good for reasons other than cost" |

| What are the 3 conditions needed for price discrimination to be possible? | 1) Firms must have a degree of monopoly power to be able to set prices 2) Must be able to identify and separate groups of people based on PED 3) Must be able to prevent market 'seepage' |

| What are the 5 benefits of price discrimination? | Firms: 1) Capture consumer surplus and turn to revenue 2) Able to make use of space capacity Consumers: 3) Can afford goods they may not have 4) Services are provided that otherwise wouldn't have been 5) Additional profit may be used to increase product quality |

| What are the 3 costs of price discrimination for the firm? | 1) Costs of keeping consumer groups apart 2) Reputation may suffer 3) Possible investigation for monopoly power |

| What are the 3 costs of price discrimination for the consumer? | 1) Lose all consumer surplus 2) Some consumers pay a high price to subsidise it for others 3) Welfare loss to consumers |

| What is a monopsony? | "A type of market structure where there is one buyer and many sellers or where one firm has significant 'buying power'. The firm has the ability to exploit its bargaining power with a supplier to negotiate lower prices in both labour and product markets." |

| Give 7 examples of barriers to entry | 1) Patents 2) Entry limit pricing (predatory pricing) 3) Cost advantages 4) Advertising and marketing 5) R&D expenditure 6) Presence of sunk costs 7) International trade restrictions |

| What is market concentration? | Is the degree to which the output of an industry is dominated by it largest producers |

| What is an oligopoly? | Where a small number of interdependent firms compete with each other. |

| What are 4 of the main characteristics of an oligopoly? | 1) Dominated by a few firms so a high concentration ratio 2) Firms are interdependent 3) High barriers to entry and exit 4) Product Differentiation |

| What are 5 things that are likely to occur in a oligopolistic market? | 1) Price Stability as they don't tend to change prices as often 2) Limit pricing 3) Predatory Pricing 4) Price War 5) Non-Price Competition |

| What is Collusion? | Firms, often operating under oligopoly conditions, working together to fix prices and avoid price wars |

| What is Overt collusion? | When firms make formal agreements between themselves to openly fix prices and restrict competition. ILLIGAL! |

| What is Tacit Collusion? | When firms co-operate without any formal agreement. Unwritten rules develop which define which firms may or may not compete. |

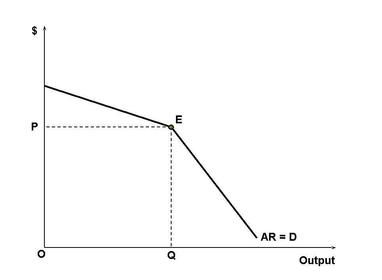

| What is the Kinked demand theory? | That oligopolists face a demand curve that is kinked at the current price, demand being significantly more elastic above the price, and more inelastic below the current price |

| What are 8 conditions that result in a successful cartel? | 1) Fewer parties involved 2) Barriers to entry protecting existing firms 3) Output can be easily monitored 4) Stable, mature industry 5) Similar production methods 6) Stable production costs 7) PED inelastic 8) Dominant firm |

| What is Game theory? | The analysis of situations in which players are interdependent |

| What is the prisoners dilemma? | A game where, given neither player needs knows the strategy of the other, the optimum strategy for each player results in a worse outcome than if they were allowed to communicate. |

| What is the difference between the MAXIMIN strategy and the MAXIMAX strategy? | The MAXIMAX is to cut price, hoping the other does the same (more optimistic) The MAXIMIN is to cut price to reduce the worst possible outcome (more cautious) BOTH CUT PRICE so it's the dominant strategy |

| Name 4 advantages of being the first mover in an industry | 1) Superior brand recognition 2) More time to perfect products 3) More customer loyalty 4) Gain from economies of scale |

| What is allocative efficiency? | When the value consumers place on a good or service is equal to the cost of resources used in production. Consumer surplus and economic welfare is maximised P = MC = AR |

| What is productive efficiency? | Output being produced at the minimum average total cost MC = AC |

| What is dynamic Efficiency? | Changes in the amount of consumer choice and the quality of goods. Is achieved by investing in R & D Downward movements in LRAC |

| Describe X-efficiency | Operating anywhere above the average cost curve |

| What is perfect competition? | A market structure where there are many buyers and sellers, where there is a freedom of entry and exit into the market, there is perfect knowledge and homogenous products |

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.