1434127

Description

Mind Map by jonesj@ellowes.dudle, updated more than 1 year ago

|

|

Created by jonesj@ellowes.dudle

over 11 years ago

|

|

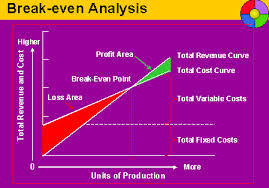

Break Even Analysis

- Fixed costs are costs that

do not change no matter

how much is produced.

- Rent, Advertising,

Interest payments on

loans.

- Rent, Advertising,

Interest payments on

loans.

- Variable costs are costs that

change depending on the

output.

- Electricity costs,

Overtime pay, Raw

Materials, Maintenance

of machinery.

- Electricity costs,

Overtime pay, Raw

Materials, Maintenance

of machinery.

- Break Even Analysis is

the point at which the

sales are exactly the

same as the costs.

- Break Even Analysis

shows us the Total costs,

Sales Revenue and

Profit.

- Fixed costs divided by selling

price-variable costs per unit.

- Graphs 1.This is done by first

working out the fixed and

variable costs at each unit of

output.

- Graphs 2. Then you fill in what

the revenue is at each stage

and add up the costs.

- Graphs 2. Then you fill in what

the revenue is at each stage

and add up the costs.

- Graphs 1.This is done by first

working out the fixed and

variable costs at each unit of

output.

- Fixed costs divided by selling

price-variable costs per unit.

- Contribution=selling

price per unit-variable

costs per unit.

- Revenue=selling

price*quantity sold.

- Margin of

safety=output-break

even point.

- Total Costs=fixed

costs + variable costs.

- Total Costs=fixed

costs + variable costs.

- Margin of

safety=output-break

even point.

- Revenue=selling

price*quantity sold.

- Break Even Analysis

shows us the Total costs,

Sales Revenue and

Profit.

- The break even point

informs the business

how many products

they need to sell so

their total revenue

equals the total costs.

- Spreadsheets/ICT is a

good way to work out the

break even point as it is a

good software to produce

graphs and charts, you can

share it via internet and its

simple to change .

- Spreadsheets/ICT is a

good way to work out the

break even point as it is a

good software to produce

graphs and charts, you can

share it via internet and its

simple to change .

- Limitations-If new rivals enter

the market or an

economic recession

starts that it can take

longer to reach the

break even point than

anticipated.

Media attachments

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.