2883010

REF:

Residential

- Cost of ownership

- stamp duty (provided)

- Buyer's stamp duty

- For properties above $360,000

- Take (AMT X 3%)-$5400

- Take (AMT X 3%)-$5400

- For properties above $360,000

- Additional Buyer's stamp duty

- For everyone except 1st time Singaporeans

- For everyone except 1st time Singaporeans

- Seller's Stamp duty

- Industrial

- Residential

- sold w/in 1 year

- means yr 0 to yr 1

- means yr 0 to yr 1

- sold w/in 1 year

- Industrial

- *Always use the higher of purchase price or valuation

- Buyer's stamp duty

- NOT IN CT

- Purchase Price

- GST

- Property Tax

- Legal and

Conveyance

Fees

- Agency

Fee/Commission

- Valuation

- Legal

Requisitions

- Operating costs

- AKA Conservacy

fee in HDB

- AKA Conservacy

fee in HDB

- Purchase Price

- stamp duty (provided)

- Calculations :)

- HDB Concessionary Loans

- LTV

- 90%

- of mkt value or vln

- whichever lower

- whichever lower

- of mkt value or vln

- 90%

- Loan interest

- 2.6%/annum

- 0.0021667/mth

- 0.0021667/mth

- 2.6%/annum

- MSR

- installment cannot exceed 30% of buyer's income

- installment cannot exceed 30% of buyer's income

- Maximum repayment period

- shorter of

- a) 25 yrs

- b) 65yrs - average age of buyers

- if pty <60 yrs

- c) balance lease - 20yrs

- c) balance lease - 20yrs

- a) 25 yrs

- shorter of

- Maximum Loan Quantum

- Lowest of

- A) Loan ceiling = LTV X VL

- 90% x VL

- 90% x VL

- B) VL - CPF in OA - CPF Grants - Half of proceeds*

- If half of proceeds <$25,000

- use

- Total proceeds -$25,000

- Total proceeds -$25,000

- use

- If half of proceeds <$25,000

- c) Loan required

- is PVOA

- i

- 0.0021667/mth

- 0.0021667/mth

- N

- Maximum repayment period (in mths)

- Maximum repayment period (in mths)

- p

- MSR

- MSR

- i

- is PVOA

- A) Loan ceiling = LTV X VL

- aka principal sum

- Lowest of

- LTV

- Residential Housing/Bank Loans

- LTV

- see table provided

- BTW

- AVG age is income weighted

- That means that eg.

Alex (27 yrs $2000) and

Bec (24 yrs $4000) The

age will be calculated as

[(2000/6000)x27yrs] +

[(4000/6000)x24yrs] =

25 years

- That means that eg.

Alex (27 yrs $2000) and

Bec (24 yrs $4000) The

age will be calculated as

[(2000/6000)x27yrs] +

[(4000/6000)x24yrs] =

25 years

- AVG age is income weighted

- BTW

- see table provided

- Loan interest

- provided in Q

- BUT

- when calculating

MAX loan

quantum, use

3.5% or provided

%, whichever is

higher

- when calculating

MAX loan

quantum, use

3.5% or provided

%, whichever is

higher

- BUT

- provided in Q

- TDSR

- total debt servicing ratio

- BY

MAS

- BY

MAS

- 60% of buyer's income

- IMPORTANT

features

- income weighted avg age

- medium term interest

rate (calc max loan)

- For residential

- 3.5% or higher

- 3.5% or higher

- For non-resi

- 4.5 % or higher

- 4.5 % or higher

- For residential

- FI to discount 30% of

buyer variable income

- Bank loan for HDB

- MSR of 30% to be CAPPED

- don't enjoy TDSR for HDB bank loan

- don't enjoy TDSR for HDB bank loan

- MSR of 30% to be CAPPED

- income weighted avg age

- total debt servicing ratio

- Maximum

repayment

period

- Absolute at 35 years

- loan period will be provided in Q :)

- Absolute at 35 years

- may be

asked

- Amount that must

be paid in cash?

- COV + MCP

- COV + MCP

- Loan quantum

- Principal Amt

aka PVAO

- Principal Amt

aka PVAO

- Monthly installment

- FVAO / N

- FVAO / N

- Max loan quantum

- similar to

HDB loan

A) and C)

- similar to

HDB loan

A) and C)

- Borrowing costs

- FVOA - PVOA

- FVOA - PVOA

- Outstanding loan

- PVOA of

remaining

years

- PVOA but

n =

remaining

yrs

- PVOA but

n =

remaining

yrs

- PVOA of

remaining

years

- Debt service ratio (%)

- borrowing cost/loan amt

- borrowing cost/loan amt

- Amount that must

be paid in cash?

- LTV

- HDB Concessionary Loans

- Terminology

- Valuation Limit (VL)

- The lower of the valuation and the purchase price

Annotations:

- Please note that the purchase price MAY be lower at times

- The lower of the valuation and the purchase price

- Cash over Valuation (COV)

- Purchase price - valuation limit

- Amount to be paid in cash when purchasing

- Purchase price - valuation limit

- Minimum Cash Payment (MCP)

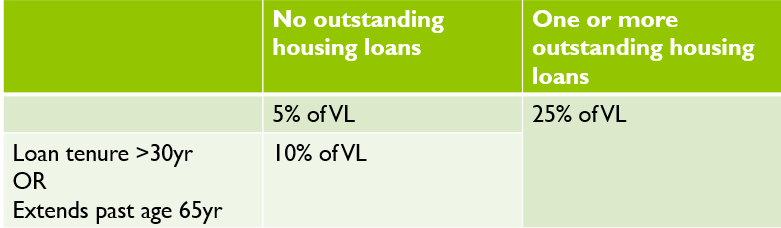

- Fixed % to pay in cash

- not covered by bank loan

- not covered by bank loan

- TABLE NOT IN EXAM

- Fixed % to pay in cash

- Loan Ceiling

- LTV x VL

- Maximum amt allowed to borrow

- Table provided in exam

- LTV x VL

- Valuation Limit (VL)

- 6 Functions of $1

- For REF

- We need to know 4

- PVOA

- Find PV given annuity

- can work backwards to find annuity given pv

- can work backwards to find annuity given pv

- Find PV given annuity

- FVOA

- Find FV given Annuity

- Find FV given Annuity

- FV = P x (1 + i)^n

- To find when installments at end of month

- PVAD

- PVOA x (1+i)

- PVOA x (1+i)

- FVAD

- FVOA x (1+i)

- FVOA x (1+i)

- PVAD

- PVOA

- We need to know 4

- For REF

- FUN

FACT: No

theory Q

in EXAMS!!

Media attachments

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.