542579

Description

Mind Map by Kati Christova, updated more than 1 year ago

|

|

Created by Kati Christova

almost 12 years ago

|

|

Fiscal Policy

- Fiscal policy is the

manipulation of government

spending, taxation and

borrowing, affecting

aggregate demand.

- Fiscal policy can

influence the current

balance and imports

through its effects on AD

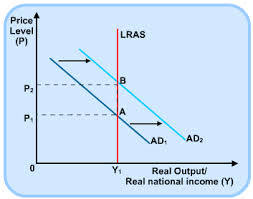

- A rise in government spending will increase

AD and shift the AD curve to the right

(assuming constant price level).

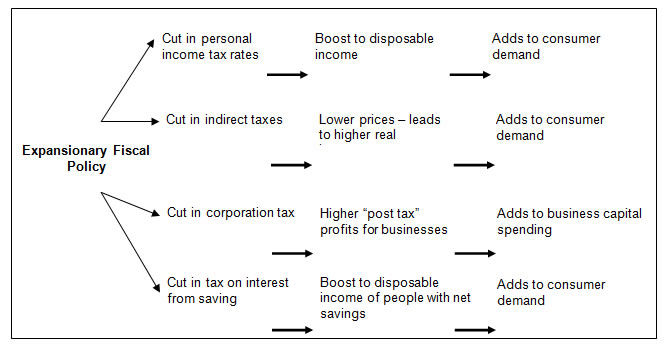

- A cut in income tax and National Insurance

Contributions will lead to increased disposable income

for households. This will lead to increased

consumption, and hence a rise in AD and a shift to the

right of the AD curve (assuming constant price level).

- The economy overheats if AD is

increased when the economy is

already at its full productive potential,

resulting in increasing inflation with

little or no increase in output

- 2006/7 due to

labour spending

- 2006/7 due to

labour spending

- The effect on AD is increased by the multiplier effect. The

multiplier effect will be larger the smaller the leakages from

the circular flow of income. In a modern economy, leakages

from savings, taxation and imports are a high proportion of

national income so the multiplier is likely to be small.

However, Keynesian economists argue it can still have a

significant impact on the output of an economy if there is

spare capacity (i.e. below full employment)

- Multiplier can be positive or negative

(when funds are withdrawn).

- Multiplier can be positive or negative

(when funds are withdrawn).

- Macroeconomic variables

- Full employment

Little or no inflation

High growth rate

External balance

(current account)

equilibrium

- Inflation

- An increase in government spending or a fall in

taxes which leads to a higher budget deficit or lower

budget surplus tends to be inflationary, because

expansionary policy leads to an increase in AD, which

leads to demand pull inflation because as the AD

curve shifts out, the price level rises.

- The size of the change in

government spending or

taxation. The larger the

change, the larger the

impact on inflation.

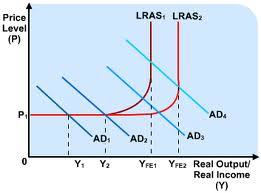

- The elasticity of the AS curve. In the short run it is relatively elastic so

a shift out will have a small impact on the price level. However, in the

long run the elasticity varies. Classical economists argue that the long

run AS curve is vertical so an increase in AD has a large impact on

prices. Keynesian economists argue that the LRAS curve is L shaped.

Where the AS curve is horizontal, there is a lot of spare capacity and

unemployment so any increase in AD will have no impact on prices.

However, when the AS curve begins to steepen, an increase in AD

leads to inflation. The nearer to full employment that the economy

operates, the greater the rise in inflation will be from a given rise in

government spending or fall in taxation.

- The size of the change in

government spending or

taxation. The larger the

change, the larger the

impact on inflation.

- An increase in government spending or a fall in

taxes which leads to a higher budget deficit or lower

budget surplus tends to be inflationary, because

expansionary policy leads to an increase in AD, which

leads to demand pull inflation because as the AD

curve shifts out, the price level rises.

- Unemployment

- A higher budget deficit or lower budget surplus tends to

reduce unemployment (in the short term) because

expansionary fiscal policy (higher government spending)

leads to an increase in AD, which leads to a higher

equilibrium of national output, and the higher the level of

national output, the lower the level of unemployment.

- The size of the

change in government

spending or taxation.

The larger the change,

the larger the impact

on AD and the labour

market.

- If LRAS is vertical an

increase in AD leads to

higher inflation and has

no effect on GDP or

unemployment.

- In the classical model,

demand side fiscal

policy cannot be used

to alter unemployment

levels in the long term.

- This is also true for the Keynesian model if

the economy is at full capacity. However, at

output levels below this, expansionary fiscal

policy will lead to a higher output and lower

unemployment. If the AS curve is horizontal,

expansionary fiscal policy can decrease

unemployment without increasing inflation.

- The size of the

change in government

spending or taxation.

The larger the change,

the larger the impact

on AD and the labour

market.

- A higher budget deficit or lower budget surplus tends to

reduce unemployment (in the short term) because

expansionary fiscal policy (higher government spending)

leads to an increase in AD, which leads to a higher

equilibrium of national output, and the higher the level of

national output, the lower the level of unemployment.

- Economic Growth

- Expansionary fiscal policy is unlikely to affect the long term growth rate

of an economy because economic growth is caused by supply side

factors such as investment, education and technology. However,

expansionary fiscal policy will increase GDP in the short run. An increase

in AD (below full capacity) will lead to a higher output. Keynesian

economists argue that expansionary fiscal policy is an appropriate policy

to use if the economy is in recession below full employment, to shift the

AD curve so that the new equilibrium is on the vertical part of the AS

curve and the economy is back to operating on its PPF. However, fiscal

policy which pushes the AD curve beyond the start of the vertical AS

curve would lead to no extra output but would be inflationary, so the

economy would be over-heating. Classical economists argue that fiscal

policy cannot be used to change real output in the long term because

the LRAS curve is vertical, so shifting AD out has no effect on output.

- shifting AD out has no effect on output.

- Multiplier can lead to

increased investment, so

LRAS may shift out

- The nature of government

spending - e.g. on training

schemes and education can

cause LRAS to shift out

- shifting AD out has no effect on output.

- Expansionary fiscal policy is unlikely to affect the long term growth rate

of an economy because economic growth is caused by supply side

factors such as investment, education and technology. However,

expansionary fiscal policy will increase GDP in the short run. An increase

in AD (below full capacity) will lead to a higher output. Keynesian

economists argue that expansionary fiscal policy is an appropriate policy

to use if the economy is in recession below full employment, to shift the

AD curve so that the new equilibrium is on the vertical part of the AS

curve and the economy is back to operating on its PPF. However, fiscal

policy which pushes the AD curve beyond the start of the vertical AS

curve would lead to no extra output but would be inflationary, so the

economy would be over-heating. Classical economists argue that fiscal

policy cannot be used to change real output in the long term because

the LRAS curve is vertical, so shifting AD out has no effect on output.

- Balance of Payments

- Expansionary fiscal policy leads to an increase in

AD, so domestic consumers and producers will

have more income, and so will import more

goods. Therefore, the current account position

will deteriorate. Tighter fiscal policy will reduce

domestic demand and imports will fall. The

current account position should then improve.

There may be other factors influencing exports

and imports. If domestic demand falls because of

tighter fiscal policy, then domestic firms may

increase their efforts to find markets overseas. A

fall in AD due to tighter fiscal policy should

moderate the rate of inflation. British goods will

become more competitive in the foreign markets,

increasing exports and reducing imports, which

improves the current account position.

- The net export effect reduces the

competitiveness of fiscal policy by offsetting

its effects. Expansionary fiscal policy leads

to higher interest rates, which cases the

currency to appreciate and exports to

decline. Contractionary fiscal policy causes

a fall in interest rates, a depreciation of the

currency and an increase in net trade

- The net export effect reduces the

competitiveness of fiscal policy by offsetting

its effects. Expansionary fiscal policy leads

to higher interest rates, which cases the

currency to appreciate and exports to

decline. Contractionary fiscal policy causes

a fall in interest rates, a depreciation of the

currency and an increase in net trade

- Government borrowing and expansionary fiscal policy tends to push

up the interest rate (monetary policy to combat the rising inflation due to

AD shifting out), increasing the returns on bonds, attracting hot money.

High demand for the currency will raise its value. The £ will strengthen,

leading to an increase in the price of exports and a fall in the price of

imports, resulting in a fall in net trade.

- Countries with high FPI (foreign portfolio

investment) can experience heightened

market volatility and currency turmoil

during times of uncertainty

- Countries with high FPI (foreign portfolio

investment) can experience heightened

market volatility and currency turmoil

during times of uncertainty

- Expansionary fiscal policy leads to an increase in

AD, so domestic consumers and producers will

have more income, and so will import more

goods. Therefore, the current account position

will deteriorate. Tighter fiscal policy will reduce

domestic demand and imports will fall. The

current account position should then improve.

There may be other factors influencing exports

and imports. If domestic demand falls because of

tighter fiscal policy, then domestic firms may

increase their efforts to find markets overseas. A

fall in AD due to tighter fiscal policy should

moderate the rate of inflation. British goods will

become more competitive in the foreign markets,

increasing exports and reducing imports, which

improves the current account position.

- The government is unlikely to be

able to achieve improvements in

one without sacrificing another

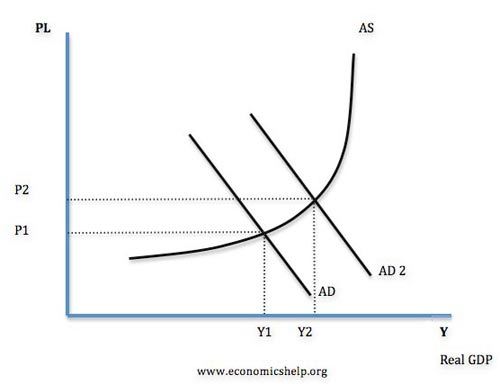

- Expanding the economy to bring it out of

recession and reduce unemployment will

lead to higher inflation

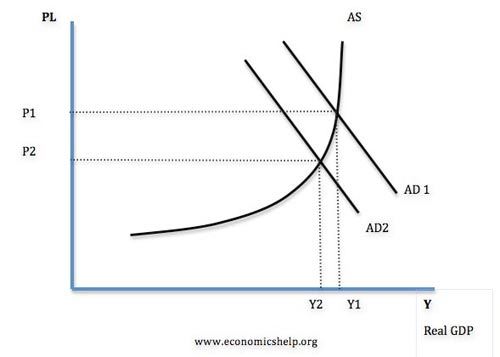

- Tightening fiscal policy to reduce

inflation will lead to higher

unemployment and lower GDP

- Contracting the domestic economy by

tightening fiscal policy to improve the

current account situation will lead to

lower inflation but higher unemployment

- Expanding the economy to bring it out of

recession and reduce unemployment will

lead to higher inflation

- Inflation

- Full employment

Little or no inflation

High growth rate

External balance

(current account)

equilibrium

- Increased confidence - firms invest

more and consumers spend more

- Reduced taxes - greater incentive to work -

more contributions to revenue and also

higher incomes so increased spending. Also

firms invest more due to lower corp tax

- A rise in government spending will increase

AD and shift the AD curve to the right

(assuming constant price level).

- Keynes vs Classical

- Classical economists argue that

fiscal policy cannot affect the level

of output in the long term, and

therefore cannot influence

unemployment but can raise inflation

- Classical economists believe that since the economy is at full capacity

in the long run, if government spending increases or fiscal policy is

loosened, inflation will increase when AD shifts out because the new

equilibrium with the LRAS curve is at a higher price level. This would be

due to a shortage of the factors of production. They would then

implement monetary policy and increase interest rates to encourage

saving and to reduce AD. Supply side factors can also be used to

control this effect because if LRAS shifts out then there will not be

inflation. Other factors that can shift our LRAS are if the multiplier

causes increased investment or just the nature of government

spending. If (like Blair) spending on education is increased then LRAS

will shift out because it affects the supply and quality of labour.

- Conservatives

- Tend to tighten fiscal policy -

reduction in the quantity and

quality of services and benefits

provided by the government

- Tend to tighten fiscal policy -

reduction in the quantity and

quality of services and benefits

provided by the government

- Classical economists believe that since the economy is at full capacity

in the long run, if government spending increases or fiscal policy is

loosened, inflation will increase when AD shifts out because the new

equilibrium with the LRAS curve is at a higher price level. This would be

due to a shortage of the factors of production. They would then

implement monetary policy and increase interest rates to encourage

saving and to reduce AD. Supply side factors can also be used to

control this effect because if LRAS shifts out then there will not be

inflation. Other factors that can shift our LRAS are if the multiplier

causes increased investment or just the nature of government

spending. If (like Blair) spending on education is increased then LRAS

will shift out because it affects the supply and quality of labour.

- Keynesian economists argue that fiscal

policy can affect both output and prices and

therefore can be used to influence both

inflation and unemployment

- Labour

- During recession if gov spending increases, this will increase

confidence, and stimulate demand and consumption and

investment and lead to a multiplier effect. This is expansionary

fiscal policy. The initial injection creates jobs and the workers

employed will spend more etc...The gov will have to run a large

deficit but these can be repaid using the fiscal dividends. During

booms, contractionary fiscal policy should be used to slow down

growth. there is a danger of over heating with higher inflation and a

higher current account deficit as the economy sucks in imports to

meet domestic demand. the government will reduce spending and

increase taxes, and the net withdrawal should put downward

pressure on consumption and investment growth and this is

supported by a negative multiplier effect.

- Fiscal policy cannot influence long term

economic growth, but it can be used to

help an economy out of a recession or

reduce demand pressures in a boom

- The budget deficit as a tool of demand management:

Keynesian economists would support the use of changing the

level of borrowing as a way of fine-tuning or managing the

level of aggregate demand. An increase in borrowing can be a

stimulus to demand when other sectors of the economy are

suffering from weak spending. The fiscal stimulus given to the

British economy during 2002-2005 has been important in

stabilizing demand and output at a time of global uncertainty.

The argument is that the government can and should use fiscal

policy to keep real national output closer to potential GDP so

that we avoid a large negative output gap. Maintaining a high

level of demand helps to sustain growth and keep

unemployment low.

- Fiscal policy cannot influence long term

economic growth, but it can be used to

help an economy out of a recession or

reduce demand pressures in a boom

- Labour

- Classical economists argue that

fiscal policy cannot affect the level

of output in the long term, and

therefore cannot influence

unemployment but can raise inflation

- Evaluating Fiscal Policy

- Crowding out - higher gov spending may lead to lower investment because there will be fewer opportunities

for private entrepreneurs to suppy goods and services. e.g. the bond market and interest rates. A budget

deficit may be funded by issuing bonds but this absorbs spending by households and firms thus reducing

spending on non-bond goods and services. Hence there is no overall increase in AD. Persuading

households and firms to buy bonds may also require an increase in the interest rat offered, placing upwards

pressure on the interest rates in the economy resulting in monetary contraction. This negative effect will be

weaker if the bonds are sold to foreigners as well as to UK households and firms.

- Some economists argue that expansionary fiscal policy (higher government

spending) will not increase AD, because the higher government spending will cause

a decrease in the size of the private sector. This is because government will have

to increase taxes or sell bonds and borrow money to finance the spending. These

reduce private consumption or investment because after buying bonds/paying

higher taxes, the private sector have lower funds for private investment. AD will

only grow slowly, if at all.

- Classical economists argue

that the govt is more

inefficient in spending money

than the private sector

therefore there will be a

decline in economic welfare

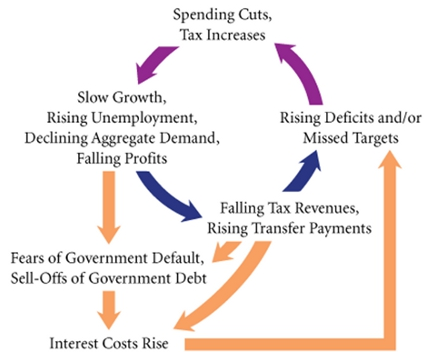

- Increased government borrowing can also

put upward pressure on interest rates. To

borrow more money the interest rate on

bonds may have to rise, causing slower

growth in the rest of the economy

- Increased government borrowing can also

put upward pressure on interest rates. To

borrow more money the interest rate on

bonds may have to rise, causing slower

growth in the rest of the economy

- In a deep recession (liquidity

trap), higher government

spending will not cause

crowding out because the

private sector saving has

increased substantially

- Monetary authorities could

counteract crowding out by

increasing the money supply to

accommodate fiscal policy

- Classical economists argue

that the govt is more

inefficient in spending money

than the private sector

therefore there will be a

decline in economic welfare

- Some economists argue that expansionary fiscal policy (higher government

spending) will not increase AD, because the higher government spending will cause

a decrease in the size of the private sector. This is because government will have

to increase taxes or sell bonds and borrow money to finance the spending. These

reduce private consumption or investment because after buying bonds/paying

higher taxes, the private sector have lower funds for private investment. AD will

only grow slowly, if at all.

- It takes time to identify a problem, implement the

policy and see the impacts - time lags.time lags

are an example of gov failure because the

cannot respond rapidly to changes in the

economy. Time lags involved are often shorter

than those for monetary policy - usually 1 year

- A situation could be that the state of the

macroeconomy suddenly changes significantly

and the policy the opposite to that required.

e.g. a previous boom has led to fiscal

contraction which by the time it takes effect

pushes the economy into deeper recession

- A situation could be that the state of the

macroeconomy suddenly changes significantly

and the policy the opposite to that required.

e.g. a previous boom has led to fiscal

contraction which by the time it takes effect

pushes the economy into deeper recession

- Classical economists - any

attempts to increase output

and reduce unemployment

using AD policy will only

create inflation

- Keynesian economists - The success of demand side policies

depends on the existing level of unemployment (spare

capacity) in the economy - the nearer we are to full

employment, the harder it is to create jobs, and the higher the

impact on price level. As AD shifts out towards the vertical

section of the AS curve, the effects on employment and output

decrease and inflation increasesmore withevery shift.

- Using fiscal policy as a means of improving supply-side performance - for example changes in corporation tax,

tax and welfare reforms to improve work incentives, to meet environmental targets - carbon taxes to reduce C02

- Using it as an

inequality

correction tool

- The extent to which fiscal policy is now an effective tool of macroeconomic

demand management - especially at a time when the conventional use of

monetary policy seems to have lost traction as a result of the credit crunch

- Increasing Taxes to reduce AD may cause disincentives to work, if this occurs there will be a

fall in productivity and AS could fall. However higher taxes do not necessarily reduce

incentives to work if the income effect dominates. Also, in a time of AD shifting in (downturn)

people will be happy to just keep their jobs so productivity may remain the same

- The effectiveness of fiscal policy will also depend upon the other components of AD, for example if

consumer confidence is very low, reducing taxes may not lead to an increase in consumer spending.

- Reduced govt spending could adversely effect public services such as public transport and education

causing market failure and social inefficiency therefore lowering living standards.

- The government may have poor information about the state of the economy and struggle to have the best information

about what the economy needs. Fiscal policy will suffer if the govt believes there is going to be a recession, increases

AD, but this forecast was wrong and the economy grows too fast, the govt action would cause inflation.

- Expansionary fiscal policy (cutting taxes and increasing G) will cause an increase in the budget deficit which has

many adverse effects. Higher budget deficit will require higher taxes in the future and may cause crowding out.

- Any change in injections may be increased by the multiplier

effect, therefore the size of the multiplier will be significant.

- Bigger multiplier = bigger impact on AD

- Bigger multiplier = bigger impact on AD

- Government spending is inefficient.

Free market economists argue that

higher government spending will

tend to be wasted on inefficient

spending projects. Also, it can then

be difficult to reduce spending in the

future because interest groups put

political pressure on maintaining

stimulus spending as permanent.

- Under certain

conditions,

expansionary fiscal

policy can lead to

higher bond yields,

increasing the cost of

debt repayments.

- It depends on other

factors in the economy. For

example, if the government

pursue expansionary fiscal

policy, but interest rates

rise and the global

economy is in a recession,

it may be insufficient to

boost demand.

- Liquidity trap

- Monetarists argue that government borrowing merely shifts resources from

private sector to public sector and doesn’t increase overall economic activity.

Increases in government borrowing will push up interest rates and crowd out

private sector investment. E.g. Japan in the 1990s where a liquidity trap was not

solved by government borrowing and a ballooning public sector debt.

- Keynesians argue that a liquidity trap makes fiscal policy very important for getting

an economy out of a recession. Since interest rates are zero but aggregate demand

is still falling, governments need to intervene to ‘crowd in’ resources left idle. The

rise in private sector saving needs to be offset by a rise in public borrowing. The

government can inject spending into the economy by increasing government

spending. This increases aggregate demand and leads to higher economic growth

without crowding out because the private sector saving has increased substantially.

- Liquidity trap: When monetary

policy becomes ineffective

because, despite zero / very low

interest rates, people want to

hold cash rather than spend or

buy liquid assets. E.g. cut in

interest rates in early 2009,

failed to revive economy.

- Keynesians respond by saying that although government borrowing might cause

crowding out in normal circumstances, in a liquidity trap, the rise in savings means

that government borrowing won’t crowd out the private sector because the private

sector resources are not being invested, just saved. Resources are effectively idle.

By stimulating economic activity the government can encourage the private sector to

start investing and spending again (hence the idea of ‘crowding in’)

- Causes

- Expectations of

deflation

- Preference for saving

- Consumers, firms and banks are pessimistic about

the future, so they look to increase their precautionary

savings and it is difficult to get them to spend. This

rise in the savings ratio means spending falls.

- Consumers, firms and banks are pessimistic about

the future, so they look to increase their precautionary

savings and it is difficult to get them to spend. This

rise in the savings ratio means spending falls.

- Banks don't want to lend

- In recessions banks are much more

reluctant to lend. Cutting the base rate

to 0% may not translate into lower

commercial bank lending rates as

banks just don't want to lend.

- They are seeking to improve their

balance sheets. They are reluctant to

lend so firms and consumers cannot

take advantage of low interest rates.

- In recessions banks are much more

reluctant to lend. Cutting the base rate

to 0% may not translate into lower

commercial bank lending rates as

banks just don't want to lend.

- Unwillingness to hold bonds

- If interest rates are zero, investors

will expect interest rates to rise

sometime. If interest rates rise, the

price of bonds falls. Therefore,

investors would rather keep cash

savings than hold bonds.

- If interest rates are zero, investors

will expect interest rates to rise

sometime. If interest rates rise, the

price of bonds falls. Therefore,

investors would rather keep cash

savings than hold bonds.

- Expectations of

deflation

- Monetarists argue that government borrowing merely shifts resources from

private sector to public sector and doesn’t increase overall economic activity.

Increases in government borrowing will push up interest rates and crowd out

private sector investment. E.g. Japan in the 1990s where a liquidity trap was not

solved by government borrowing and a ballooning public sector debt.

- If there is concern over

the state of government

finances, the government

may not be able to borrow

to finance fiscal policy.

Countries in the Eurozone

experienced this problem

in the 2008-13 recession.

- The success of fiscal

policy depends on the

state of the economy.

Fiscal policy is most

effective in a deep

recession where monetary

policy is insufficient to

boost demand.

- If expansionary fiscal policy occurs during

periods of deflation it is likely to fail to boost

overall aggregate demand. It is only when

people expect a period of moderate inflation

that real interest rates fall and the fiscal policy

will be effective in boosting spending.

- Responsiveness of changes

in taxes to changes in GDP

- What kind of fiscal

policy - spending on

what? Cuts in taxes

for whom?

- estimating the

magnitude of the

effects is hard

- estimating the

magnitude of the

effects is hard

- Fiscal policy is ineffective

when investment is very

sensitive to interest rates and

when consumers attempt to

offset the actions of the

government (e.g. saving a tax

cut, or increasing their saving

when higher government

spending leads to expectations

of higher taxes in the future)

- Crowding out - higher gov spending may lead to lower investment because there will be fewer opportunities

for private entrepreneurs to suppy goods and services. e.g. the bond market and interest rates. A budget

deficit may be funded by issuing bonds but this absorbs spending by households and firms thus reducing

spending on non-bond goods and services. Hence there is no overall increase in AD. Persuading

households and firms to buy bonds may also require an increase in the interest rat offered, placing upwards

pressure on the interest rates in the economy resulting in monetary contraction. This negative effect will be

weaker if the bonds are sold to foreigners as well as to UK households and firms.

- Government Budget

- Borrowing

- When a government runs a budget

deficit, it has to borrow money.

Borrowing of the public sector over a

period of time is called the public sector

net cash requirement (PSNCR).

- An increase in government

spending or a fall in taxes which

increases the budget deficit or

reduces the budget surplus is

called Expansionary Fiscal

Policy. Fiscal policy is said to

loosen as a result of these.

- Expansionary fiscal

policy - fiscal policy

used to increase AD

- 2010 Coalition Government

- lower taxes but reduced

provision of services

- Expansionary fiscal

policy - fiscal policy

used to increase AD

- There is a deficit

when revenue is

lower than spending

- Deficit is around 6%

of GDP but peaked at

11% in 2010

- Deficit is amount

borrowed yearly

- Sustained deficit means the

economy is not self-sustaining

- Sustained deficit means the

economy is not self-sustaining

- The deficit can be funded by

borrowing. Governments do this by

issuing bonds which are a form of IOU.

The funds rasied from selling these

bonds can be used for capital spending

projects or to fund current expenditure

(unsustainable). The total value of

outstanding bonds is the national debt.

- The accumulation of the total money

owed is the national debt. It is about

89% of GDP (due to rescuing the

banks in 2008). 40% of GDP is the

sustainable level of national debt.

- $1.3 trillion ($46bn

due to interest)

- $1.3 trillion ($46bn

due to interest)

- A budget deficit can have positive

macroeconomic effects in the long run if

it is used to finance extra capital

spending that leads to an increase in the

stock of national assets, improving the

supply-side capacity of the economy.

- The accumulation of the total money

owed is the national debt. It is about

89% of GDP (due to rescuing the

banks in 2008). 40% of GDP is the

sustainable level of national debt.

- However, if the budget deficit rises to a

higher level, the government may have to

offer higher interest rates to attract buyers.

- In the long run, higher

government borrowing today

may mean that taxes will have to

rise in the future and this would

put a squeeze on spending by

private sector businesses and

millions of households.

- This means that the

Gov has to spend

more each year in

debt-interest

payments.

- There is an opportunity cost because

interest payments might be used in more

productive ways, for example an

increase in spending on health services.

It also represents a transfer of income

from people and businesses that pay

taxes to those who hold government

debt and cause a redistribution of

income and wealth in the economy

- There is an opportunity cost because

interest payments might be used in more

productive ways, for example an

increase in spending on health services.

It also represents a transfer of income

from people and businesses that pay

taxes to those who hold government

debt and cause a redistribution of

income and wealth in the economy

- In the long run, higher

government borrowing today

may mean that taxes will have to

rise in the future and this would

put a squeeze on spending by

private sector businesses and

millions of households.

- Deficit is around 6%

of GDP but peaked at

11% in 2010

- Should not occur

at full employment

- An increase in government

spending or a fall in taxes which

increases the budget deficit or

reduces the budget surplus is

called Expansionary Fiscal

Policy. Fiscal policy is said to

loosen as a result of these.

- When a government runs a budget surplus,

there is negative PSNCR as there is no need

to borrow money. This allows the government

to pay off part of its national debt.

- Decreased government spending or

increased taxes, which lead to a

higher budget surplus or lower deficit

is tightening of fiscal policy.

- Austerity measures

- Austerity measures are

generally unpopular

because they tend to

lower the quantity and

quality of services and

benefits provided by the

government.

- Stabilised prices when inflation is getting out of control

- Stabilised prices when inflation is getting out of control

- Austerity measures are

generally unpopular

because they tend to

lower the quantity and

quality of services and

benefits provided by the

government.

- Contractionary/Deflationary policy

- Consumers spend less due to

higher taxes (lowers disposable

income) and low confidence.

Also increase disincentive to

work so productivity and

unemployment increases. The

government spends less. Firms

invest less due to higher taxes

and reduced confidence

- AD shifts inwards

- AD shifts inwards

- Austerity measures

- Using the surplus to decrease debt may

cause interest rates to fall, stimulating

spending, which could be inflationary. It is

better for the funds to just sit

- Decreased government spending or

increased taxes, which lead to a

higher budget surplus or lower deficit

is tightening of fiscal policy.

- When a government runs a budget

deficit, it has to borrow money.

Borrowing of the public sector over a

period of time is called the public sector

net cash requirement (PSNCR).

- Tax

- Corporation Tax

- Lowering the corporation tax

leads to increased investment

and FDI. For example, Ireland's

rate is 12% and this attracted

companies like Amazon and

Google. It also encourages

investment and risk taking

- However too much

confidence can be a bad

thing since people start

going for too risky/low

return investments

simply because they can,

and money can be lost

- However too much

confidence can be a bad

thing since people start

going for too risky/low

return investments

simply because they can,

and money can be lost

- Lowering the corporation tax

leads to increased investment

and FDI. For example, Ireland's

rate is 12% and this attracted

companies like Amazon and

Google. It also encourages

investment and risk taking

- Income tax

- Progressive - as

income rises, the

tax rate rises

- Thresholds - 20% for those

earning less than £30,000. 40%

for earnings between £30,000

and £150,000 and 45% for

earnings of above £150,000

- Guaranteed income

£10,000

- Gov can control this

guaranteed portion and

therefore consumption?

- Reduce the tax free allowance but

keep the tax rates low e.g. 10% OR

raise the allowance (allowing people

to keep more of their income) but

increase taxes to say 30%

- Reduce the tax free allowance but

keep the tax rates low e.g. 10% OR

raise the allowance (allowing people

to keep more of their income) but

increase taxes to say 30%

- Gov can control this

guaranteed portion and

therefore consumption?

- Guaranteed income

£10,000

- Helps reduce inequality

- if tax was regressive

(flat rate) the poorest

would be hit hardest

- Thresholds - 20% for those

earning less than £30,000. 40%

for earnings between £30,000

and £150,000 and 45% for

earnings of above £150,000

- High income tax deters

people from working.

Also the higher skilled

and higher income works

look abroad for better

salaries post-tax under

less punitive tax regimes

- brain drain effect.

- Progressive - as

income rises, the

tax rate rises

- Effects depend on responsiveness of

changes in tax to changes in spending

/investment etc - proportion of income etc...

- Corporation Tax

- Spending

- There are 2 types of government spending. Capital

spending increases the productive capacity of the

economy, shifting LRAS to the right. It includes

investment in infrastructure and building more schools

and hospitals. Current spending is the day-to-day

running of the public sector and includes purchasing

raw materials for school supplies/drugs, paying wages

etc...When an economy is in recession, shifting out

LRAS will have little effect because the economy is not

a full employment, so capital spending should be done

when the economy is booming, so that loosening fiscal

policy in a recession does not cause inflation - there is

room for AD to shift out before it becomes inflationary.

- Unrealistic for the budget to

balance because there is

additional capital spending.

Therefore the rule should be that

current spending must equal tax

receipts over the economic cycle.

- Unrealistic for the budget to

balance because there is

additional capital spending.

Therefore the rule should be that

current spending must equal tax

receipts over the economic cycle.

- The golden rule states that the budget should be balanced

over an economic cycle. As the economy moves from a boom

to a downturn or recession, government spending should

increase and tax revenue fall. This is called fiscal drag and it

has a stabilising effect on the economy. As unemployment

rises in a downturn, the government budget moves into a

deficit as the injection provided outweighs the withdrawal

through taxes, creating a net injection and increasing AD. As

growth outstrips trend growth, there is likely to be an

increase in tax receipts and a fall in government spending as

fewer households require benefits. This is called a fiscal

dividend - the benefit to the budget position of strong short

term growth. The net withdrawal slows the circular flow of

income and may dampen the impact of growth. However by

removing the peaks and troughs of the economic cycle, the

impact on living standards is lower.

- Actual budget surplus/deficit

may differ greatly from full

employment estimates

- Full employment budget measures

what the gov deficit/surplus would

be with the current rates of gov

spending and taxation, if the

economy was at full employment

- Full employment budget measures

what the gov deficit/surplus would

be with the current rates of gov

spending and taxation, if the

economy was at full employment

- There are 2 types of government spending. Capital

spending increases the productive capacity of the

economy, shifting LRAS to the right. It includes

investment in infrastructure and building more schools

and hospitals. Current spending is the day-to-day

running of the public sector and includes purchasing

raw materials for school supplies/drugs, paying wages

etc...When an economy is in recession, shifting out

LRAS will have little effect because the economy is not

a full employment, so capital spending should be done

when the economy is booming, so that loosening fiscal

policy in a recession does not cause inflation - there is

room for AD to shift out before it becomes inflationary.

- Borrowing

- Government spending OR taxation

- If there is concern over

unmet social needs or

infrastructure, higher

government spending

during recessions and

higher taxes during

inflationary times is better

- If the government is too

large or inefficient, lower

taxes during recessions

and lower government

spending during inflationary

periods is better

- If there is concern over

unmet social needs or

infrastructure, higher

government spending

during recessions and

higher taxes during

inflationary times is better

Media attachments

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.