Description

|

|

Created by britneysoll

over 10 years ago

|

|

Page 1

Financial Markets, Instruments, and Interest Rates

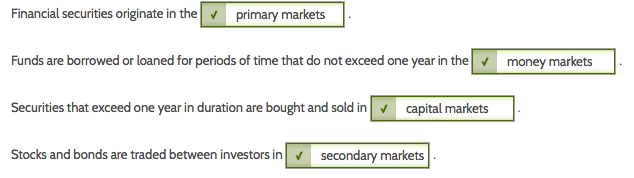

Financial Markets Introduction Imagine that you have saved $2000 to take a trip around the world next year. Where could you invest the money in the meantime? You want the greatest return and least risk. If you understand the financial market, you can make good choices. Financial markets match with money, lenders, to those without, borrowers. These markets allow new businesses to start and existing companies to expand. They allow individual investors to grow their money. It is important to understand the differences between the various markets, including the money markets, capital market, primary market, and secondary market. It is also important to understand the differences between organized exchanges and over-the-counter markets.

Financial Markets and Institutions Financial markets are the conduit through which money flows between savers and borrowers. Without financial markets, how would your grandmother in Oregon find a manufacturing firm in South Florida who needs to borrow some money from her?Through financial markets, you can invest in a mutual fund that buys debt (bonds) issued by a business. You do not have to know the business owner, nor does the business owner have to know you. The existence of the financial market make these connections possible.If you have some money saved in your bank account, at some point you need to decide if you want a little higher return. So you withdraw your accumulated savings and call your stock broker, who places the money in a small company bond mutual fund. The small company bond fund has previously bough bonds issued by a manufacturing firm. This process was initiated when the owner of the manufacturing firm approached and investment banking firm and had them put together a bond issue. The manufacturing firm took the bond proceeds and used them for expansion. The investment banking firm sold the bonds to a number of investors, including the fund manager of the manufacturing firm bond fund where you invest your money. This entire transaction, in which your surplus funds found their way to the small business in south Florida, occurred in the financial markets. The players included the bank where you first accumulated your funds, the broker who sold you the small bond mutual fund, the small bond mutual fund that purchased the bonds for its portfolio, and the investment banker who put the bond issue together for the manufacturing firm in south Florida.Stock Broker is a licensed financial professional who buys and sells investments for clients. Capital Markets Capital Markets are financial markets where securities that exceed on-year in maturity are bough and sold. This market includes the stock market, bond markets, and long-term loans. Keeping in mind that financial markets do not necessarily have a physical location. Some prominent financial markets, like the New York Stock Exchange (NYSE) do have physical locations, but many are simply computer networks where securities are bought and sold. Primary vs Secondary Markets Primary markets are the markets where financial security is originated. For example, when the small firm in south Florida sells bonds to an investment banking firm, that transaction is a primary market transaction. The only time a firm receives funds is when the security (stock or bond) is used in the primary market. Every transaction after that point occurs in the secondary market. In secondary markets, stock and bonds are traded between investors. Wal-Mart does not get a single penny when Wal- Mart stock changes hands on the NYSE. This market is merely on investor selling its Wal-Mart stock to another investor. So why is this market so important to Wal-Mart?These active secondary markets determine that stock price. If investors did not have an active secondary market that provided instant liquidity, the most would be reluctant to be stock. This is the reason why secondary markets are important to all firms.

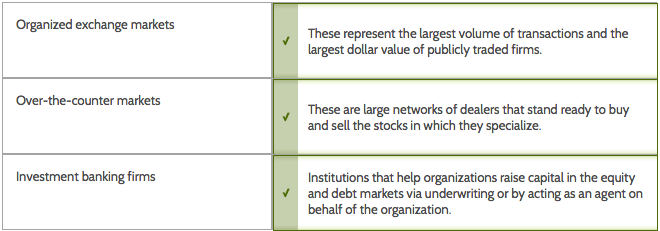

Money Markets The distinction between money markets and capital markets is based on time. Money markets are markets in which funds are borrowed or loaned for periods of time that do not exceed one year. The short-term securities used in this market include U.S Treasury bills, negotiable certificates of deposit, bankers' acceptances, commercial paper, and others. These financial instruments are typically very low risk because they are issued by the most creditworthy issuers. Because of their low risk, they typically offer low returns relative to other securities. As a financial manager, there may be times when you need to invest money for a very short period of time by using money markets. You may also use the money markets as a low-cost source of short-term funds if your firm is creditworthy enough to attract buyers. Many auto financing companies use commercial paper as a low-cost source of short-term funds. Commercial paper is a very short-term bond that allows a company to borrow at lower rates than long term. As long as the commercial paper does not have a maturity that exceeds 270 days, it does not have to be registered with Securities Exchange Commission (SEC). However, it takes a very strong, recognizable company to be able to sell commercial paper, because it bypasses SEC scrutiny. Organized Exchanges and Over-the-Counter Markets Organized exchanges include many of the ones recognizable in physical locations. Examples include the NYSE and the American Stock Exchange (AMEX). These markets represent the largest volume of transactions and the largest dollar value of publicly traded firms. Firms trading on the organized exchanges are capable of meeting the stricter listing requirements imposed for each exchange. The larger firms benefit from wider recognition and more active trading that provides investors wit greater liquidity.Liquidity refers to the ease that some assets can be converted to cash without significant loss of value. In contrast, the OTC market is not one physical location but, instead, a large network of dealers that stand ready to buy and sell the stocks in which it specializes. Normally, this market is not as liquid as the organized exchanges. The typical firm is smaller and not able to meet the stricter listing requirements with regard to revenue, profitability, the number of shareholders, and other requirements imposed by the organized exchanges. However, there are some notable exceptions. Microsoft Corporation trades on the OTC market. The NASDAQ provides real-time price data and allows the larger firms traded via the NASDAQ to have the same instant liquidity and pricing as stocks listed on the organized exchanges. Many of the very small OTC firms do not have this benefit. These firms start out on the smaller markets and progress upward as they grow and meet the more stringent listing requirements.

{kind=link}

{kind=link}

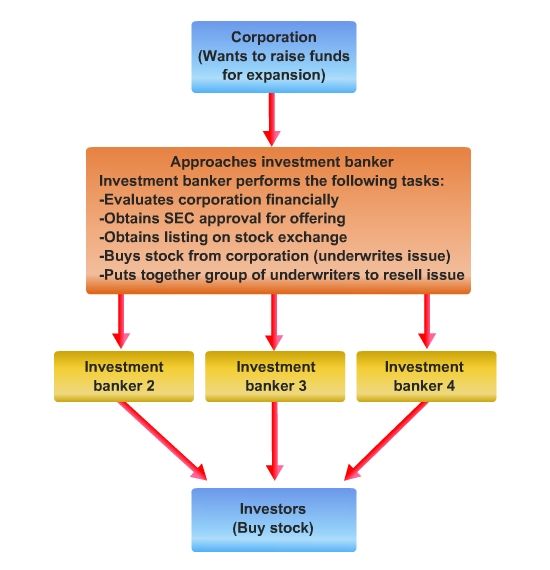

Equity and Debt Five Grain Inc., a fictional bread-baking company, needs an expensive state-of-the-art oven system. It decides to raise money for equipment by selling part of itself. In other words, it issues common stock, which in effect, sells a fraction of the company to others. Five Grain Inc. can also sell bonds or other short-term debt to raise money. Equity vs debt The way a firm pays for its productive assets is via a combination of equity and debt. For example, if you want to buy a $1 000 000 piece of equipment, you use equity (pay for it with money raised via sale of ownership), debt (borrowed money), or some combination of both. When a firm issues stock in the primary market, it is raising equity. Firms can then take this money and use it for their business needs. The other option open is to borrow money. Firms can borrow via a bank loan or they may opt to sell bonds or other short-term debt, such as commercial paper. Common Stock Each share of common stock represents fractional ownership in the company. If a firm has only 100 shares of common stock issued and outstanding, then each share represents 1% ownership of the company. An investor with 10 shares would own 10% of the company and would be entitled to 10% of any cash or stock distribution the company makes. Most publicly traded companies have millions of shares of common stock outstanding, each share represents a very small fractional ownership of the firm. A firm issues stock by approaching and investment banker. The banker evaluates the financial condition and business model of the company that wishes to issue equity, and makes some assessment of value. At that point, the investment banking firm may opt to underwrite the issue, which is basically a direct purchase of the stock. The investment banking firms gets the stock issue registered with SEC, and gets the issue listed on either an organized exchange or the OTC market. At that point, the underwriter begins selling or placing the issue. This transaction is called the initial public offering. Common Stock Negotiation At this point, the issuing firm has its money and is no longer involved in the process. The underwriter has some placement options and may sell the stock through a syndicate or group of other underwriters. The underwriters make their money on the difference between what they paid the firm for the stock and what they sell it for. Sometimes, firms that want to raise capital allow underwriters to bid on equity using a competitive process. At other times, the price may simply be negotiated with one investment banking firm. This choice is dictated by the firm's prospects and visibility. Firms with high visibility (high-profile) owners can typically negotiate better deals than firms without name recognition.At times, the investment banking firm may opt to put the issue together for a fee and then sell the stock on a commission basis. In this case, the issue is not underwritten or purchased outright. The investment banking firm may be successful in selling all or part of the stock, but only guarantees to give their best effort to place the issue. Corporate Bond Features A bond will have a fixed maturity date, and a coupon rate. A fixed maturity date is the date at which the bod is scheduled to be repaid in full, which is established at issuance. The coupon rate is the suggested rate of interest paid on the bond. Debenture Bond The typical corporate bond is insecure and is known as a debenture bond. A debenture bond is an unsecured bond or a bond that is not backed by any assets. If the company opts to pledge assets as collateral against the debt, it is dubbed a mortgage bond. In the case of a mortgage bond, the creditors have some assets to sell if the company defaults on the debt. Mortgage bonds are therefore, not as sky as debentures, and allow the firm to pay a lower coupon rate. Sweeteners Because most corporate bonds are debentures, there are other features firms can use as sweeteners that allow them to pay lower coupon rates. Some bonds are convertible to a fixed number of shares of common stock after a certain period time. This feature allows bondholders to receive a constant return in the form of coupon payments, but it also gives them the option to convert to equity at some point. These conversion can only occur if the company's stock price increases beyond the conversion price. At other times, companies may attach warrants that allow the investor to use some fixed number of warrants to buy shares of stock at some point. Both these options give bondholders the potential to participate in ownership, and allow the firm to pay lower interest rates.

Equity on a Small Scale Let's think about equity on a smaller scale. If you want a $1000 television set, and you only have $600, you could ask your roommate if he would pay the other $400. This makes you co-owners of the television, and you control the remote with 60% ownership. Debt on a Smaller Scale You prefer to own the television set outright. You approach your uncle about loaning you the money until you graduate from college in two years. You promise to make interest payments annually (5%) and pay the amount in full six months after graduation. You have effectively issued a bond with a $400 face value and a 5% coupon rate that matures in 2.5 years. A television set is not a productive asset, but the options via which you raised the money are similar to what a company might go through when it needs funds. It cab borrow money or sell equity (ownership). A firm that owns productive assets paid for it by raising money through selling fractional ownership in the business or they borrowed the money. Ask the questions: What do I own? How did I pay for it?

{kind=link}

Corporate Bonds Companies have numbers options when issuing bonds, and process is almost identical to the process with issuing stock. However, in this case, the underwriter guide the firm through getting the bonds rated by an independent rating agency, and also discusses features that will impact the coupon rate the firm must pay on the debt.Bond issues are submitted to independent debt rating agencies. These firms evaluate the creditworthiness of the issuing firm and assign the bond with a rating that indicates their assessment at default risk. The higher the bond is rated, the lower the interest the firm has to pay. Investors want to be compensated for assuming a higher level of risk with a higher interest rate. Therefore, the underwriter uses this rating coupled with current market rates of interest to determine the bond's coupon rate, or the rate of interest it will pay annually.

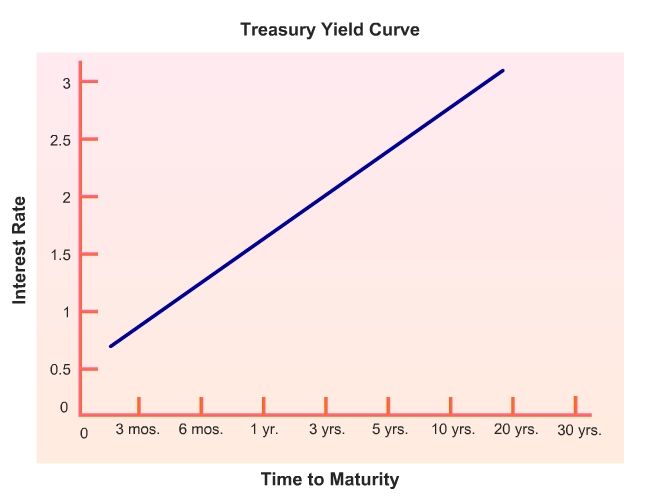

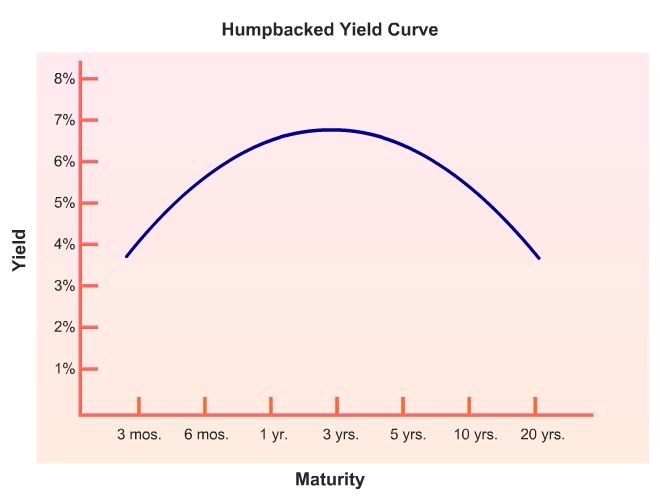

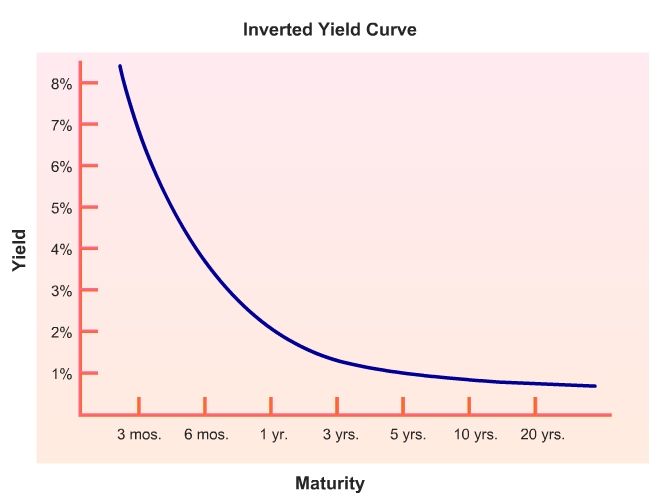

Interest Rates and the Yield CurveOne factor that impacts interest rates is the length of time to maturity. In finance, we call this relationship between the interest rates and maturity the term structure of interest rates. The graph representation of the term structure of interest rates is called the yield curve. Yield CurvesTo construct the field curve and see the pure relationship between the interest rate and maturity, we need to remove all other extraneous factors that may impact the interest rates. The best way to do this is to use U.S Treasury debt. The U.S Treasury issues debt of various maturities from the very short term to the very long term. Because it is backed by the federal government, we have removed all the noise factors associated with using different issuers. To construct the field curve, you merely plot the field on the vertical axis and the maturity on the horizontal axis. The typical, or normal, held curve is upward sloping and to the right, in other words, the longer the maturity continues, the higher the curve. Interest Rate TheoriesInterest rates are affected by a combination of future expectations, premiums to forgo liquidity, and the supply and demand for money of different maturities. There are three dominant theories as to the shape of the yield curve. Unbiased Expectations TheoryUnbiased expectations theory postulates that the shape of the yield curve is the result of investors expectations of future interest rates. If the investors the believe the interest rates will be higher in the future, they demand higher interest rates on longer term debt to tie p their money for that length of time. The normal yield curve is the graphical representation of this expectation. If investors believe interest rates will fall in the future, you see lower rates on longer term debt. An inverted yield curve is the graphical representation of this expectation. Liquidity PreferenceThis theory states that investors require some interest rate premium to induce them to tie up their money for longer periods of time. There is some value to being liquid because there is a higher level of risk when you tie up your money for longer periods of time.What if interest rates increase and you've locked in a low return? What happens to the value of your investment? It will decline as the interest rates rise. To compensate for this additional risk associated with longer term investments (lack of liquidity), investors require additional compensation in the form of higher interest rates. You can see that this theory can't explain an inverted or humpback yield curve. Market SegmentationMarket segmentation theory attempts to explain the term structure of interest rates through supply and demand. Investors and firms have different time preferences. Some investors want to lock up their excess funds for short periods of time. Some firms may only need funds for short periods of time. Businesses that are cyclical and need funds to create inventory during a particular season. Those businesses may want to borrow funds for six months, and they anticipate cynical sales generating the surplus cash needed to repay those short-term loans. These to market participants, short term lenders and the short-term borrowers are only interested in that segment of the market in which funds are borrowed and landed for six-month periods. Market segmentation theory postulates that the interest rate is determined by the supply and demand for funds in that market segment.

{kind=link}

{kind=link}

{kind=link}

Rates of ReturnA distinction needs to be made between nominal and real rates of return. The nominal rate of return is the stated or quoted rate of interest. For example, the stated rate of return on 10-year U.S. Treasury securities may be 5% However, the real return to an investor depends on the rate of inflation. If inflation is currently running at 3%, then investors are only getting an approximate 2% real return. In other words, these investors will only experience a 2% increase in purchasing power at maturity because inflation erodes some of the dollar's value. Understanding the difference between nominal rates and real rate is critical because rational investors do not lend money at a nominal rate that is not greater than the rate of inflation. If they did, they would lose purchasing power. The money you repaid at maturity would not buy as much as the original amount. Investors are therefore more interested in the real return.Nominal turn = real retune + inflation premiumReal return = nominal return - inflation premium

Want to create your own Notes for free with GoConqr? Learn more.