Description

Page 1

Financial Accounting Standards Board Codification: The codification is a compilation and reorganization of all GAAP sources : Referred to as Accounting Standards Codification (ASC).

{kind=link}

Page 2

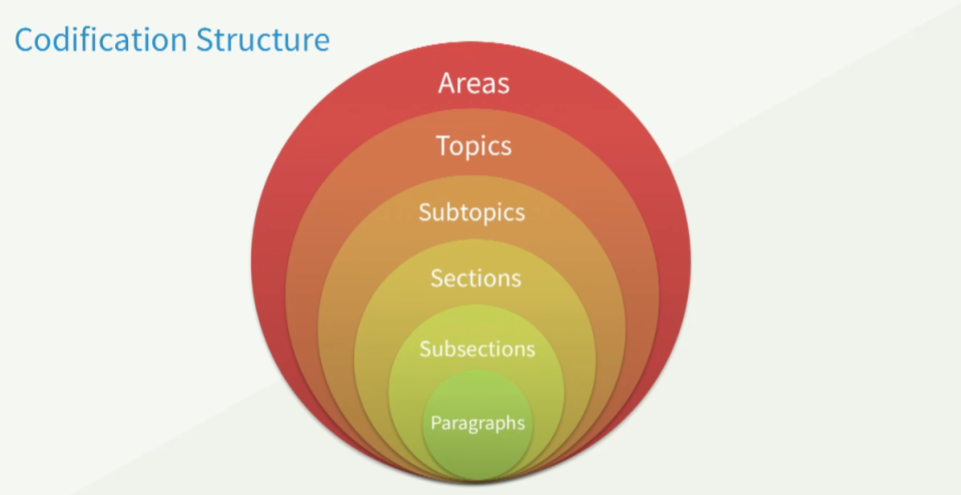

Goals of the Codification: The FASB Codification Research System is the online, real-time database by which users access the Codification. Updating the Codification: Accounting Standards Updates (ASUs) 1. Summarize key aspects of the update, 2. detail how the codification will change, and 3. explain the basis for the update. Vehicle to update. Codification Structure: Areas, Topics, Subtopics, Sections, Subsections, Paragraphs. Areas: The highest level in the Codification is the area, of which there are nine, each with a specific numeric identifier General Principles (100) Presentation (200) (does not address recognition or measurement) Assets (300) Liabilities (400) Equity (500) Revenue (600) Expenses (700) Broad Transactions (800) (transaction involving more than one area such as interest, and subsequent events); Industry (900) (special industry accounting) Topics: There are approximately 90 topics across the nine areas. For example, all asset topics are within 300-399. Subtopics: There is at lease one subtopic within each topic.Sections: Each subtopic has the following 16 sections with the associated numeric identifier: 00 Status05 Overview and background10 Objectives15 Scope and Scope Exceptions20 Glossary25 Recognition30 Initial Measurement35 Subsequent Measurement40 Derecognition50 Disclosure55 Implementation Guidance and Illustrations60 Relationships65 Transition and Open Effective Date Information70 Grandfathered Guidance75 XBRL DefinitionsSubsections: In some cases, a section is divided into subsections to facilitate the exposition. These are not numbered.Paragraphs: The actual accounting standard material is provided in paragraphs within sections or subsections. Industry: Area 900 holds industry topics and contains only the guidance that is not otherwise applicable in the other eight areas.Areas excluded from the Codification include: Other Comprehensive basis of accounting, Cash Basis Accounting, Income Tax Basis accounting, Regulatory Accounting Principles (e.g. Insurance), and Governmental Accounting Standards.

0 comments

Want to create your own Notes for free with GoConqr? Learn more.