2397409

Description

Flashcards by Jessie Coulston, updated more than 1 year ago

|

|

Created by Jessie Coulston

almost 11 years ago

|

|

| Question | Answer |

| Service Cost | increase in the employer's obligation attributed to employee service during the period |

| Interest | interest accrued on the obligation during the period (balance at the beginning of the period multiplied by the interest rate) |

| Changes in the PBO included currently | Service cost and Interest |

| Changes in the PBO delayed recognition | Losses or gains on the PBO and prior service cost |

| Losses or (gains) on the PBO | increase or (decreases) in the estimate of the PBO from revisions in underlying assumptions |

| Prior service cost | increase in the employer's obligation due to giving credit to employees for years of service provided before the pension plan is amended (or initiated) |

| Changes in plan assets included currently | Return on the plan assets |

| Changes in plan assets delayed recognition in Income | Losses or gains on the plan assets |

| Return on the plan assets | increase in value of plan assets during the period, adjusted for employer contributions and benefits paid to retirees. Actual return adjusted for losses and gains on the plan assets |

| Losses or gains on the plan assets | return on plan assets lower or higher than expected |

| Cash contributions | payments into the fund by the employer |

| Pension expense | Service cost + interest cost -Expected return on the plan assets +Amortization of prior service cost +Amortization of net loss |

| Corridor rule | if net loss (gain) > 10% of PBO or plan assets, the excess is amortized to pension expense |

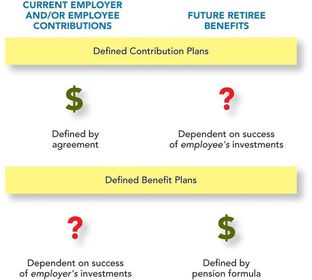

| Nature of pension plans (image) | |

| The fundamental components of a defined benefit pension plan are: (3) | 1) The employer's obligation to pay retirement benefits in the future. 2) The plan assets set aside by the employer from which to pay the retirement benefits in the future. 3) The periodic expense of having a pension plan. |

| Defined benefit pension plan characteristics | 1) Employer is committed to specified retirement benefits 2) Retire. ben. are based on a formula that considers years of service, compensation level, and age 3) Employer bears all risk of pension fund performance |

| Defined contribution pension plan characteristics | 1) Contributions are defined by agreement. 2) Employer deposits an agreed-upon amount into an employee-directed investment fund. 3) Employee bears all risk of pension fund performance. |

| Three different was to measure pension obligation: | 1. Accum. Benefit Obligation: PV of est. retirement benefits earned so far by employees, estimated by plugging existing compensation levels into the pension formula 2. Vested Benefit Obligation: part that plan participants are entitled to receive regardless of their continued employment 3. Projected benefit obligation: PV of estimated retirement benefits earned so far by employees, estimated by plugging projected compensation levels into the pension formula |

| Steps to calculate PBO | 1. Use the pension formula (including a projection of future salary levels) to determine the retirement benefits. 2. Find the PV of the retirement benefits as of the retirement date 3. Find the PV of retirement benefits at the current date |

| PBO can change due to: | 1. Service cost 2. Interest cost 3. Prior service cost 4. Loss (gain) on PBO 5. Retiree benefits paid |

| Plan assets can change due to: | 1. Return on plan assets- dividends, interest, market price appreciation 2. Cash contributions 3. Retiree benefits paid |

| A trustee is usually hired who: | 1. Accepts employer contributions 2. Invests the contributions 3. Accumulates the earnings on the investment 4. Pays benefits from the plan assets to retired employees or their beneficiaries |

| Overfunded | Market value of plan assets exceeds the actuarial PV of all benefits earned by participants |

| Underfunded | Market value of plan assets is below the actuarial PV of all benefits earned by participants |

| Valuation allowance | A valuation allowance is needed if it is more likely than not that some portion or all of a deferred tax asset will not be realized |

| Operating loss carryback | an operating loss carryback can be deducted from taxable income in the two prior years, creating a refund of taxes paid for those years |

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.