515481

Description

Mind Map by Harshad Karia, updated more than 1 year ago

|

|

Created by Harshad Karia

almost 12 years ago

|

|

Break-even Analysis

- Nature Costs

- Fixed Costs

- Semi- variable

- Variable

- Fixed Costs

- Calculations of break even

- Formula

- Selling Price (Per Unit) - Variable Costs (Per Unit) = Contribution per Unit

- Fixed Costs / Contribution per Unit = Break-even point

- Fixed Costs / Contribution per Unit = Break-even point

- Selling Price (Per Unit) - Variable Costs (Per Unit) = Contribution per Unit

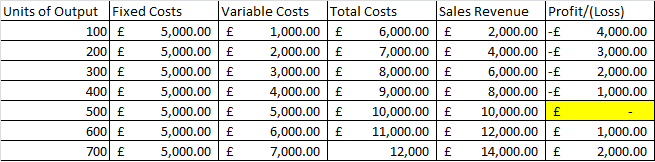

- Table Method

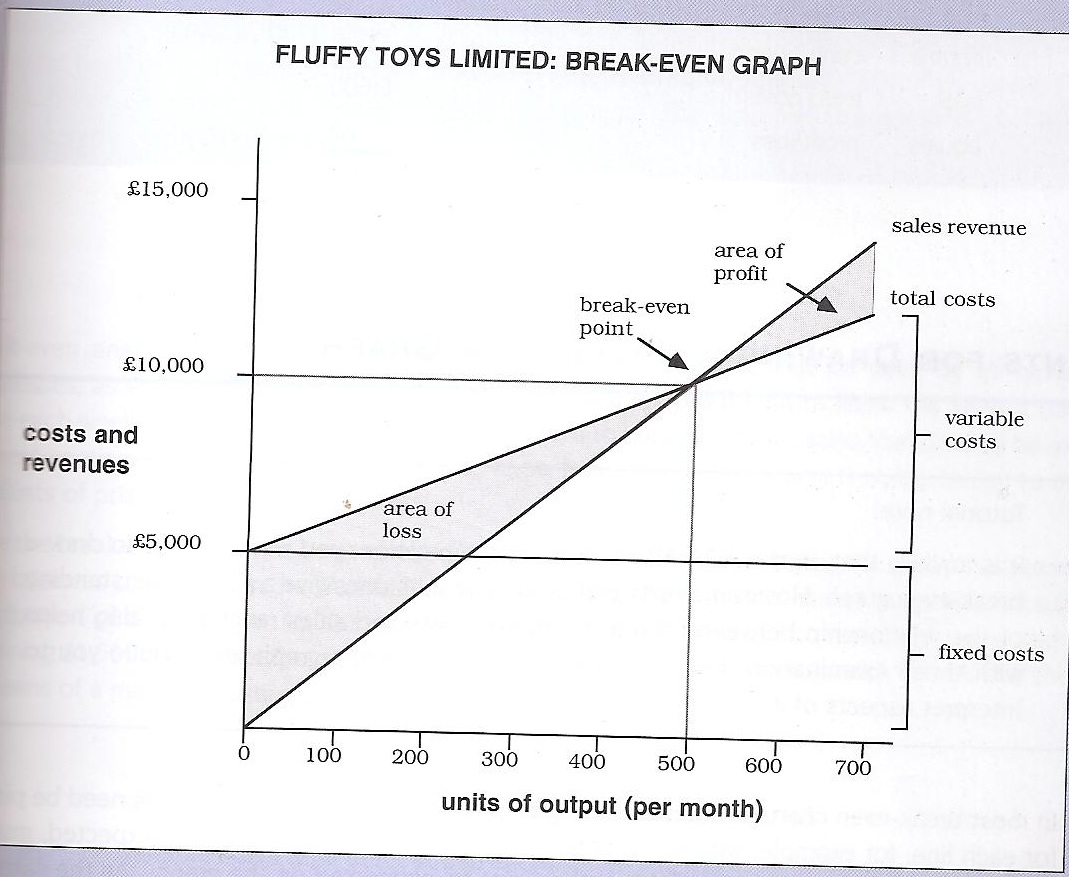

- Graph Method

- Formula

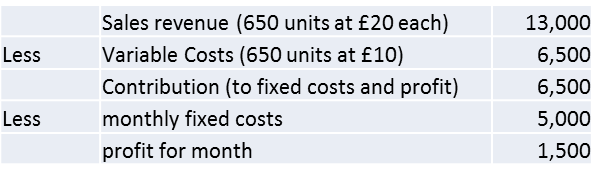

- Interpretation of break-even

- The information provided

can help interpret what the

profit would be after selling

a certain amount of units.

- The information provided

can help interpret what the

profit would be after selling

a certain amount of units.

- Margin of Safety

- The amount by which sales exceed the break-even point.

- No. of units : Sales volume - break-even point (units)

- Sales Revenue amount : Sales volume - break-even

point (units) x Selling price

- Percentage : (current output - break-even output) (100) /

Current output

- The amount by which sales exceed the break-even point.

- Target Profit

- Calculating the 'Target Profit' shows the

amount of output that needs to be sold in

order to give a certain amount of profit

- (fixed costs + target profit) / Contribution per unit

- Calculating the 'Target Profit' shows the

amount of output that needs to be sold in

order to give a certain amount of profit

- Contribution sales/Profit Volume ratio

- Expresses the amount of contribution in relation to the amount of the selling price

- Formula

- Contribution / Selling Price

- Contribution / Selling Price

- Calculated on the basis of a single unit of production or for the whole business

- If Fixed costs are known, we can use the CS ratio to find the sales value at which

the business breaks-even, or the sales value to give a target amount of profit

- Expresses the amount of contribution in relation to the amount of the selling price

- Dis-advantages/ Limitations

- Based on estimates

- No semi-variables

- External factors not considered, such as

economy, interest rates, the rate of inflation, etc

- Relationship between sales revenue, variable costs and

fixed costs remains the same at all levels of production.

Only useful if the product is going sell in sufficient

quantities

- Difficult to make calculations for a mix of products, therefore it

require separate calculations for every different type of product

- costs and revenue are expressed in terms of straight lines,

however the relationship is not always so. Selling prices vary at

different quantities sold; in similar way, variable costs alter at

different levels as advantage is taken of the lower prices to be

gained from bulk buying, and/or more efficient production methods

- Fixed costs do not remain fixed at all levels of

output

- You can not forecast from the graph of what could

be obtained by selling more units, therefore not

allowing you to extrapolate the graph or

calculations

- The profit or loss shown by the graph or calculations is

probably only true for figures close to current output levels -

the more that output changes from the current figures, the

less accurate will be the expected profit or loss

- Based on estimates

- Advantages

- Useful for a new business in order establish the level of sales that must be

achieved to reach break-even point.

- Useful for a new business in order establish the level of sales that must be

achieved to reach break-even point.

- When to use Break-even analysis?

- Before starting a new business

- The calculation of break-even point is important in

order to see the level of sales needed by the

business in order to cover costs, or to make

particular levels of profit. The feasibility of achieving the

level can be considered by the owner of the business,

and other parties such as the bank manager.

- The calculation of break-even point is important in

order to see the level of sales needed by the

business in order to cover costs, or to make

particular levels of profit. The feasibility of achieving the

level can be considered by the owner of the business,

and other parties such as the bank manager.

- When making changes within a business

- The cost of a major change will need to be

considered by the owners and/or managers.

Eg. a large increase in production will. most

likely, affect the balance between fixed and

variable costs. Break-even analysis will be

used as part of the planning process to

ensure that the business remains profitable.

- The cost of a major change will need to be

considered by the owners and/or managers.

Eg. a large increase in production will. most

likely, affect the balance between fixed and

variable costs. Break-even analysis will be

used as part of the planning process to

ensure that the business remains profitable.

- To measure profits and losses

- Within the limitations of break-even analysis, profits and

losses can be estimated at different levels of output from

current production. (Remember that this can be done

only where the new output is close to current levels and

where there is no major change to the structure of costs

- ie. it is not possible to extrapolate)

- Within the limitations of break-even analysis, profits and

losses can be estimated at different levels of output from

current production. (Remember that this can be done

only where the new output is close to current levels and

where there is no major change to the structure of costs

- ie. it is not possible to extrapolate)

- To answer 'what if?' questions

- Questions such as 'what if sales fall by 10%?' and 'what if fixed costs increase

by £1,000?' can be answered - in part at least - by break-even analysis. The

effect on the profitability of the business can be seen, subject to the limitations.

A question such as 'what if sales increase by 300 per cent?' is a fundamental

change that it can only be answered by exclaiming the effect on the nature of

the fixed and variable costs and then re-calculating the break-even point.

- Questions such as 'what if sales fall by 10%?' and 'what if fixed costs increase

by £1,000?' can be answered - in part at least - by break-even analysis. The

effect on the profitability of the business can be seen, subject to the limitations.

A question such as 'what if sales increase by 300 per cent?' is a fundamental

change that it can only be answered by exclaiming the effect on the nature of

the fixed and variable costs and then re-calculating the break-even point.

- To evaluate alternative viewpoints

- There are often different ways of production; this is particularly true of a

manufacturing business. For example, a product could be made, either by a

labour-intense process, with a large number of employees supported by basic

machinery, or buy using expensive machinery in an automated process with

very few employees. In the first case, the cost structure will be high variable

costs (labour) and low fixed costs (depreciation of machinery). In the second,

there will be low variable costs and high fixed costs. Break-even analysis can

be used to examine the relationship between the costs which are likely to show

a low break-even point in the first case, and a high break-even point in the

second. In this way, the management of the business is a guided by

break-even analysis; management will also need to know the likely sales

figures, and the availability of money with which to buy the machinery.

- There are often different ways of production; this is particularly true of a

manufacturing business. For example, a product could be made, either by a

labour-intense process, with a large number of employees supported by basic

machinery, or buy using expensive machinery in an automated process with

very few employees. In the first case, the cost structure will be high variable

costs (labour) and low fixed costs (depreciation of machinery). In the second,

there will be low variable costs and high fixed costs. Break-even analysis can

be used to examine the relationship between the costs which are likely to show

a low break-even point in the first case, and a high break-even point in the

second. In this way, the management of the business is a guided by

break-even analysis; management will also need to know the likely sales

figures, and the availability of money with which to buy the machinery.

- Before starting a new business

Media attachments

{kind=link}

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.