1728989

Description

Quiz by Beatriz Peregrina Viñolo, updated more than 1 year ago

|

|

Created by Beatriz Peregrina Viñolo

over 10 years ago

|

|

Question 1

Question

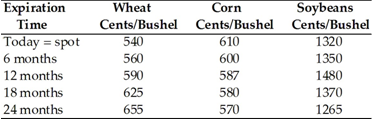

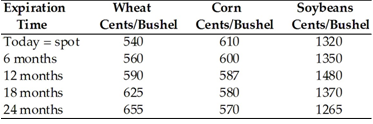

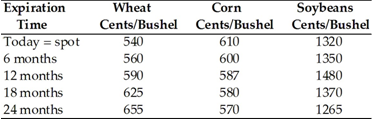

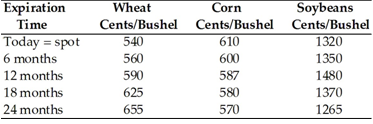

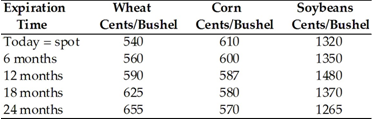

Refer to the table 6.1. What is the approximate annualized lease rate on the 12-month corn forward contract?

Image:

tabla_6.1.PNG (image/PNG)

{kind=link}

Answer

-

0.00%

-

2.25%

-

3.92%

-

7.84%

Question 2

Question

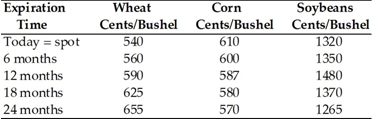

Refer to the table 6.1. What is the approximate annualized lease rate on the 18-month soybean forward contract?

Image:

tabla_6.1.PNG (image/PNG)

{kind=link}

Answer

-

0.69%

-

1.52%

-

2.69%

-

3.31%

Question 3

Question

Refer to the table 6.1. If wheat farmers expect a return of 8.0% on their investment in wheat, what is the approximate implied increase in wheat commodity prices over the next 6 months?

Image:

tabla_6.1.PNG (image/PNG)

{kind=link}

Answer

-

3.75%

-

4.59%

-

5.26%

-

6.37%

Question 4

Question

Refer to the table 6.1. Which of the following terms most accurately describes the forward curve for soybeans over the next two years?

Image:

tabla_6.1.PNG (image/PNG)

{kind=link}

Answer

-

Contango

-

Backwardation

-

Contango and backwardation

-

None of the above

Question 5

Question

Refer to the table 6.1. Given a lease rate of 7.0% on the 24-month corn forward contract, what is the approximate potential arbitrage profit per contract?

Image:

tabla_6.1.PNG (image/PNG)

{kind=link}

Answer

-

3.68 cents

-

4.48 cents

-

5.84 cents

-

6.90 cents

Question 6

Question

Refer to the table 6.1. The lease rate on the 6-month soybean contract is 0.35%. What is the implied annual storage cost if the cost is continuously paid and proportional?

Image:

tabla_6.1.PNG (image/PNG)

{kind=link}

Answer

-

0.84%

-

1.62%

-

2.30%

-

4.0%

Question 7

Question

The spot price of gasoline is 258 cents per gallon and the annualized risk free interest rate is 4.0%. Given a lease rate of 1.0%, a continuously paid storage rate of 0.5%, and a convenience yield of 0.75%, what is the no-arbitrage price range of a 1-year forward contract (in cents)?

Answer

-

265.19 to 267.19

-

258 to 265.19

-

258 to 267.19

-

247.16 to 265.19

Question 8

Question

Nine-month gold futures are trading for $1565 per ounce. The spot price is $1509 per ounce. LIBOR during each of the upcoming 4 quarters is listed as 1.04%, 1.22%, 1.30%, and 1.35%, respectively. Calculate the 9-month lease rate on the futures contract.

Answer

-

2.4%

-

2.1%

-

1.3%

-

0.0%

Question 9

Question

Forward prices for gold, in dollars per ounce, for the next five years are 1350, 1400, 1560, 1675, and 1756, respectively. A mine can be opened for 3 years at a cost of $2,000. Annual mining costs are a constant $500 and interest rates are 5.0%. When should the mine be opened to maximize NPV?

Answer

-

Year 1

-

Year 2

-

Year 3

-

Never

Question 10

Question

The 6-month futures price for oil is $96.60 per barrel (or 2.30 cents per gallon). The 6-month futures prices for gasoline and heating oil are 2.50 cents and 2.15 cents, respectively. What is the gross margin on a simple 3-2-1 crack spread?

Answer

-

$0.25

-

$0.35

-

$0.54

-

$0.68

Question 11

Question

The spot price of corn is $5.85 per bushel. The opportunity cost of capital for an investor is 0.5% per month. If storage costs of $0.04 per bushel per month are factored in, all else being equal, what is the likely price of a 4-month forward contract?

Answer

-

$5.808

-

$5.736

-

$5.968

-

$6.006

Question 12

Question

The spot price of corn is $5.82 per bushel. The opportunity cost of capital for an investor is 0.6% per month. If storage costs of $0.03 per bushel per month are factored in, all else being equal, what is the future value of storage costs over a 6-month period?

Answer

-

$0.1534

-

$0.1684

-

$0.1772

-

$0.1827

Question 13

Question

Oil is selling at a spot price of $42.00 per barrel. Oil can be stored at a cost of $0.42 per barrel per month. The opportunity cost of capital is 7.2% per year (or 0.6% per month). What is the gain or loss realized by an oil refinery that floats its exposure and purchases oil on the spot market in 2 months at a price of $43.00 per barrel, instead of hedging with a forward contract?

Answer

-

$0.35 gain

-

$0.35 loss

-

$1.00 gain

-

$1.00 loss

0 comments

Want to create your own Quizzes for free with GoConqr? Learn more.