17587845

Description

Flashcards by Anastasia Mazierski, updated more than 1 year ago

|

|

Created by Anastasia Mazierski

over 6 years ago

|

|

| Question | Answer |

| Who are the main users of financial statements? | Lenders Borrowers Shareholders Investors Employees Government Public Lenders |

| What is the distinction between auditing and accounting? | Accounting is recording, classifying and summarizing of economic events to provide financial information for decision making Auditors focus on determining whether recorded information properly reflects the economic events that occurred during the accounting period |

| What is auditing | Auditors focus on determining whether recorded information properly reflects the economic events that occurred in the accounting period In addition to understanding accounting, auditors must possess expertise in the accumulation and interpretation of audit evidence |

| What is accounting? | The recording, classifying and summarizing of economic events to provide financial information for decision making |

| What makes information useful? | RAVTRUC Relevant accessible verifiable Timely Reliable Understadable complete |

| What is meant by determining the degree of correspondence between information and established criteria? | To do an audit, information must be in a verifiable form and some standards by which the auditor can evaluate the information. Determining the degree of correspondence between info and criteria is determining whether a given set of info is in accordance with the criteria |

| What are the major causes of information risk? | Remoteness of information Biases and motives of the provider Voluminous data Existence of complex exchange transactions |

| How can information risk be reduced? | User verifies the information User shares the info risk with management Audited financial statements are provided |

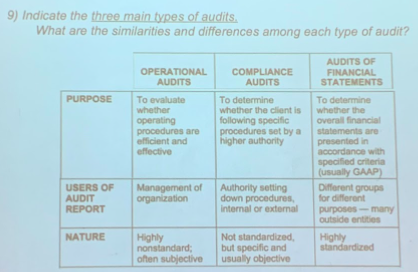

| What are the three main types of audit? | Operational Compliance Audits of financial statements |

| What are the similarities and differences among each type of audit? | |

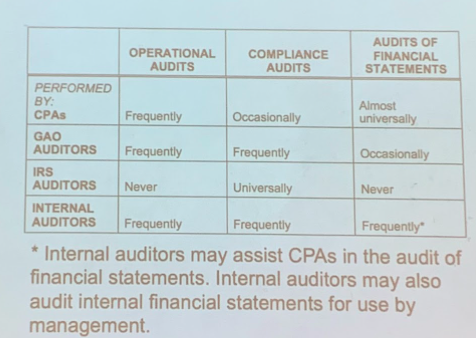

| What are the similarities among each type of auditors? | |

| What changes in accounting and business operations over the last decade have increased the need for independent audits? | Increased global activities: multiple product lines and transaction locations; foreign exchange affects transactions Complex accounting and exchange transactions: increasing use of derivatives and hedging activities; increasingly complex accounting standards More complex information systems: possibly millions of transactions processed daily through on-line and traditional sales channels; voluminous data requires interpretation |

| Information risk | Reflects the possibility that the information upon which the business risk decision was made was inaccurate, a likely cause is inaccurate financial statements |

| Auditors nightmare is | material misstatement |

| Assurance service | An independent professional service to improve the quality of information for decision makers |

| Attestation service | A form of assurance service in which the CPA firm issues a report about the reliability of an assertion that is the responsibility of another party |

| Audit services | A form of attestation service in which the auditor expresses a written conclusion about the degree of correspondence between information and established criteria |

| Different forms of evidence a tax auditor will need in the audit of the tax return of a company | Electronic and documentary data about transactions Written and electronic communication with outsiders observations by the auditor Oral testimony of the client |

| Rules of accounting | Criteria used by the auditor for evaluating presentation of economic events for financial statements |

| What are the advantages and disadvantages of the 3 different ways to reduce information risk? | |

| What are the 4 categories of attestations service? | Audit of historical financial statements Audit of internal control over financial reporting Review of historical financial statements Other attestation services that may be applied to a broad range of subject matter |

| Similarities of financial statement audits, operational audits and compliance audits | Each type of audit involves accumulating and evaluating evidence about information to ascertain and report on the degree of correspondence between the information and established criteria and/or procedures, rules and regulations |

| Differences of financial statement audits, operational audits and compliance audits | The information being examined and criteria used to evaluate the information |

| What are the three primary requirements to become a CPA | Educational: an undergrad or grad degree in accounting Uniform CPA examination requirement: 4 part computer exam incl. auditing/attestation/financial accounting/reporting/regulation/business environment and concepts Experience requirement: varies state to state |

| What is the distinction between auditing and accounting? | Accounting: recording, classifying and summarizing of economic events to provide information for decision making Auditing: focus on determine whether information recorded properly reflects the economic events that occurred in that accounting period In addition to understanding accounting, auditors must expertise in the accumulation and interpretation of audit evidence |

{kind=link}

{kind=link}

{kind=link}

0 comments

Want to create your own Flashcards for free with GoConqr? Learn more.