1337398

Economics

- Foundation of Economics

- Scarcity

- Lack of resources. Emphasis

that there are not enough

resources to meet all people's

wants. As a result choices

has to be made.

- Waste is expensive therefore they

have to use resources efficiently.

- Lack of resources. Emphasis

that there are not enough

resources to meet all people's

wants. As a result choices

has to be made.

- Opportunity cost

- "The next best alternative

forgone when an economic

decision is made.

- you have 100$ and you want

to buy a bag (98$) and a dress

(95$).You can't buy both so if

you buy the bag the dress will

be the opportunity cost.

- you have 100$ and you want

to buy a bag (98$) and a dress

(95$).You can't buy both so if

you buy the bag the dress will

be the opportunity cost.

- "The next best alternative

forgone when an economic

decision is made.

- Factors Of Productions

- 2.Labour

- These are the

human resources

that are used to

produce goods

and services.

- Workers.

- un-skilled

- semi-skilled

- Skilled

- un-skilled

- Workers.

- These are the

human resources

that are used to

produce goods

and services.

- 4.Enterprise

- is the organisation where all

factors of production are

together. Entrepreneur are

risk takers.

- is the organisation where all

factors of production are

together. Entrepreneur are

risk takers.

- These refer to 4 resources

that allows an economy to

produce its output.

- 1.Land

- It's the earth's natural resources

- trees

- oil

- Land itself

- pay a rent

- pay a rent

- trees

- It's the earth's natural resources

- 3.Capital

- Refers to the

investment in

manufactured

resources. AND.

investment in human

capita.

- Machinery,

factories and

roads

- Education and

health care

- Machinery,

factories and

roads

- Refers to the

investment in

manufactured

resources. AND.

investment in human

capita.

- 2.Labour

- Scarcity

- Demand

- Definition

- Is the willingness and ability of

consumers to buy a quantity of a good

or service at a certain price. (in a given time period

- Is the willingness and ability of

consumers to buy a quantity of a good

or service at a certain price. (in a given time period

- Markets

- Define as a process or institute in which

producers and consumers interact in order to

sell or buy a good or service.

- Define as a process or institute in which

producers and consumers interact in order to

sell or buy a good or service.

- The Law of Demand

- Definition

- As the price of a product falls, the quantity

demand of a product increases and when the

price of a product increases, the quantity

demanded falls.

- As the price of a product falls, the quantity

demand of a product increases and when the

price of a product increases, the quantity

demanded falls.

- Definition

- Demand Schedule

- Is a table giving the quantities

demanded at a range of

prices.

- Is a table giving the quantities

demanded at a range of

prices.

- Demand Curves

- It plots the information on a graph with the price on the Y-axis

and the quantity demanded on the X-axis.

- A change in the price of the product will lead to a change in the quantity

demanded of the product. There is a movement along the demand curve.

- Downward Slope

- It plots the information on a graph with the price on the Y-axis

and the quantity demanded on the X-axis.

- The Increase in Demand is due to:

- Income

- When the price of a good falls, people

will have have an increase in their

real-life income. Likely to buy more.

- When the price of a good falls, people

will have have an increase in their

real-life income. Likely to buy more.

- Substitution Effect

- When the price of a product falls the product

will become more attractive to people than

other similar products whose prices have stayed the

same.

- When the price of a product falls the product

will become more attractive to people than

other similar products whose prices have stayed the

same.

- Income

- Non Price Determinant of Demand:

- Income

- Inferior Goods

- As income rises, demand for the

product will fall as the consumers

starts to buy higher priced substitutes

instead.

- Public Transport

- Butter and Margarine

- Rice and bread.

- As income rises, the demand curve will

shift to the left.

- own brand products at the

supermarket

- As income rises, demand for the

product will fall as the consumers

starts to buy higher priced substitutes

instead.

- 2 types of products to consider when looking at how

a change in income affects the demand for a

product.

- Normal Goods

- As income rises, the demand for the

product will also rise.

- As income rises, the

demand curve for normal

goods will shift -----> to the

right.

- Size of shift depends on the good.

- As income rises, the

demand curve for normal

goods will shift -----> to the

right.

- As income rises, the demand for the

product will also rise.

- Inferior Goods

- Leads to a shift in the demand curve

either to the right or to the left.

- Make the ceteris paribus assumption

- Make the ceteris paribus assumption

- The price of other goods

- Substitutes

- If products are substitutes for each other, then a change in

the price of one of the product will lead to change in the

demand for the other product.

- Coca Cola and Pepsi

- Chicken and Beef

- If there is a fall in the price of chicken, there

will be an increase in the quantity demanded

of chicken and a fall in the demand for beef.

- If there is a fall in the price of chicken, there

will be an increase in the quantity demanded

of chicken and a fall in the demand for beef.

- This could lead to a

movement along the

demand curve for chicken.

- And a shift to the

left of the demand

curve for beef.

- And a shift to the

left of the demand

curve for beef.

- If products are substitutes for each other, then a change in

the price of one of the product will lead to change in the

demand for the other product.

- Complements

- Products purchased together.

- Cars and petrol

- DVD player and DVD's

- Tennis racket and tennis ball

- Cars and petrol

- If the price of one product change it will lead to a change in

demand for for the other products.

- If there is a fall in the price of DVD players, then there

will be an increase in the quantity demanded of DVD

player and also an increase in the demand for DVD's,

which are complements.

- If there is a fall in the price of DVD players, then there

will be an increase in the quantity demanded of DVD

player and also an increase in the demand for DVD's,

which are complements.

- Products purchased together.

- Unrelated Goods

- Products that have nothing in common

- A change in the price of one product

will have no effect upon the demand

for the other good

- An increase in the price of rice will have no

impact upon the demand for clothes

- An increase in the price of rice will have no

impact upon the demand for clothes

- Products that have nothing in common

- Substitutes

- Tastes and Preferences

- Firms tries to attempt to influence tastes by marketing, so

that they can shift the demand curve for their product to the

right

- Firms tries to attempt to influence tastes by marketing, so

that they can shift the demand curve for their product to the

right

- Other Factors

- The Size of the Population

- pop size increases = demand

for most products will increase.

- Shift to the right

- Shift to the right

- pop size increases = demand

for most products will increase.

- Age structure of the population

- Ageing pop

- Demand more for walking sticks and nursing homes.

- Demand more for walking sticks and nursing homes.

- Young pop

- Demand more for schools, teachers, clothes shops.

- Demand more for schools, teachers, clothes shops.

- Ageing pop

- The Size of the Population

- Income

- Definition

- Supply

- Definition

- The willingness and ability of a

producer to produce a quantity

of goods or service at a certain

price (in given time period).

- The willingness and ability of a

producer to produce a quantity

of goods or service at a certain

price (in given time period).

- The law of Supply.

- States as the price of

a product rise, the

quantity supplied will

usually increase,

ceteris paribus.

- The curve will normally

slope upwards.

- Can be illustrated by

schedule or a supply

curve

- States as the price of

a product rise, the

quantity supplied will

usually increase,

ceteris paribus.

- The Non-Price Determinant of Supply:

- 2.The Price of Other Goods.

- Producers often have a

choice as to what they

are going to supply.

- example: A producer of roller skates

may be able to produce stake boards

with minimal change in facilities.

- If the price of the skateboards

rise, because there is more

demand for them, then it may be

that the producers will be

attracted by higher prices and

come to supply more

skateboards and fewer roller

skates.

- There is a movement along the supply

curve for skateboards.

- There will also be a fall in

supply for roller skates at all

prices

- And the supply will shift to the left , even though

the price has not changed there is a fall in supply.

- And the supply will shift to the left , even though

the price has not changed there is a fall in supply.

- There is a movement along the supply

curve for skateboards.

- If the price of the skateboards

rise, because there is more

demand for them, then it may be

that the producers will be

attracted by higher prices and

come to supply more

skateboards and fewer roller

skates.

- example: A producer of roller skates

may be able to produce stake boards

with minimal change in facilities.

- Producers often have a

choice as to what they

are going to supply.

- 1. Cost of

Factors of

Production.

- An increase price in wages

- Will lead to a

fewer supply at all prices

- It will shift the supply curve

to the left.

- It will shift the supply curve

to the left.

- Will lead to a

fewer supply at all prices

- An increase price in wages

- 3. State Of Technology.

- Improvements in tech

will increase in supply.

- Improves productivity.

- Productivity- os the amount

of output per unit of input.

- Productivity- os the amount

of output per unit of input.

- Lead to a shift to the right.

- Improves productivity.

- Improvements in tech

will increase in supply.

- 4. Government Intervention.

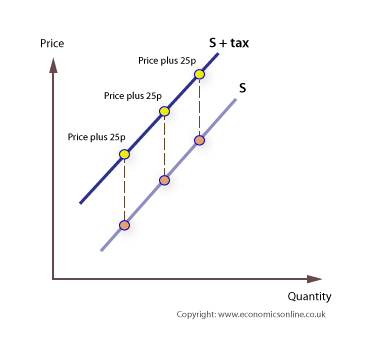

- Inderect Taxes

- Taxes on goods and services that are added to the price of a product.

- Increase in indirect tax will lead to increase the

cost of production.

- Increase in indirect tax will lead to increase the

cost of production.

- Shift the supply curve to move upwards by the amount of the indirect tax.

- Taxes on goods and services that are added to the price of a product.

- Governments inverse in the

markets in ways that alter the

supply.

- Regulations

- Applying a rules and regulations to protect

consumers or the workers.

- Extra cost to the firm

- eg. cigarettes and alcohol

- Extra cost to the firm

- Applying a rules and regulations to protect

consumers or the workers.

- Supply Shocks

- normal events that disrupt the supply of goods or services

- Positive

- Shift to the right.

- discover minerals in soil

- Shift to the right.

- Negative.

- Shift to the left

- Natural disasters

- Man-made environmental disaster

- Conflicts such as wars

- Shift to the left

- Positive

- normal events that disrupt the supply of goods or services

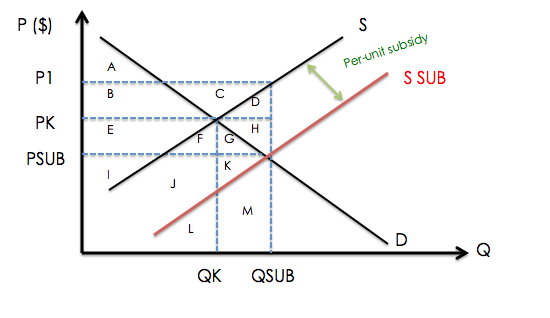

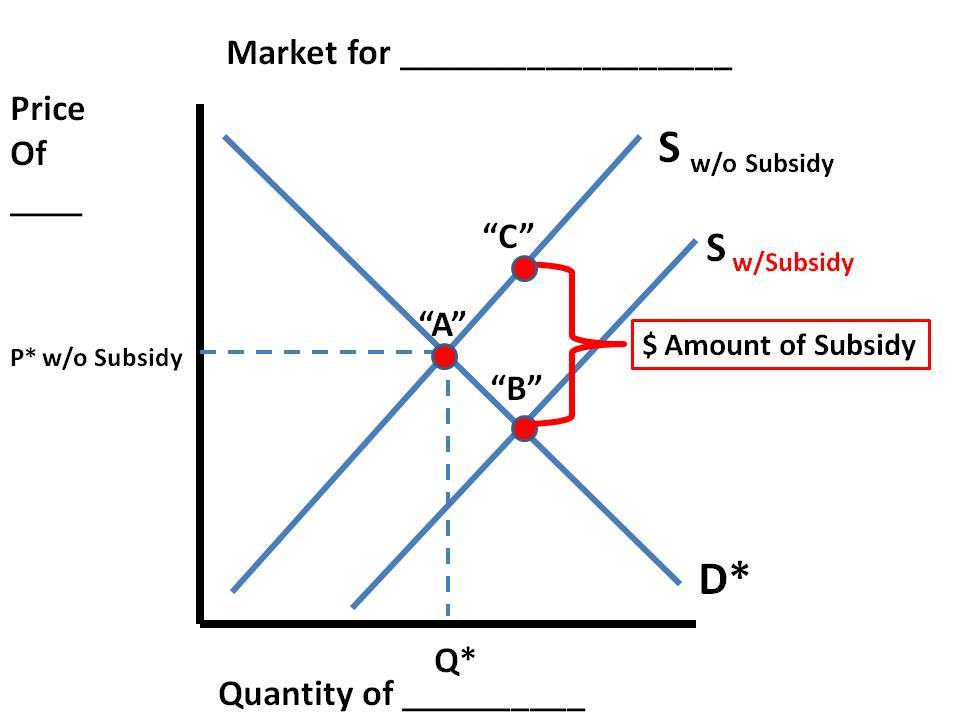

- Subsidies

- The government pays producer to make more of the good.

- Reduces the cost of production

- Shif supply curve to move downwards by the amount of subsidy.

- More will be supplied

- Reduces the cost of production

- The government pays producer to make more of the good.

- Inderect Taxes

- 2.The Price of Other Goods.

- Definition

- Production Possibilities

Curves/Production

Possibilities Frontier.

- 1. PPC shows the maximum

combinations of goods and

services that can be produced by

an economy in a given time

period.

- 2. Shows that there is a limit to

what a country can produce.

Scarcity of economic resources

limits output to points on or below

the PPC

- 2. Shows that there is a limit to

what a country can produce.

Scarcity of economic resources

limits output to points on or below

the PPC

- Shifts

- Left

- 1. Shows a decrease in its

productivity capacity.

- Caused by:

- War and natural disasters.

- War and natural disasters.

- Caused by:

- 1. Shows a decrease in its

productivity capacity.

- Right

- 1. Shows a country's

ability to produce more

goods and services.

- Caused by:

- Improvements in the

quality and quantity of

the factors of production.

- Reduce water to gain and

raise more land.

- Reduce water to gain and

raise more land.

- Improvements in the

quality and quantity of

the factors of production.

- Caused by:

- 1. Shows a country's

ability to produce more

goods and services.

- Economic Growth

- A rise in the productive potential.

- An increase in the output of goods and services

- An increase in the output of goods and services

- A rise in the productive potential.

- Left

- 1. PPC shows the maximum

combinations of goods and

services that can be produced by

an economy in a given time

period.

Media attachments

{kind=link}

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.