16395140

Description

Mind Map by William Kim, updated more than 1 year ago

|

|

Created by William Kim

over 5 years ago

|

|

PERFECTLY COMPETITIVE MARKETS

- EXAMPLES

- Rice Farms

- Farming Activity

- Poultry Farming

- Rice Farms

- Price Taker

- Firms are Restrained from raising its price because consumers will find another competitor in the market with lower prices

- Many Firms

- Many buyers and firms exist to create the larger market

- Many buyers and firms exist to create the larger market

- Many Identical Products

- Relative Ease in Market Entry

- Meaning there are no barriers or walls preventing anyone from entering the market

- Meaning there are no barriers or walls preventing anyone from entering the market

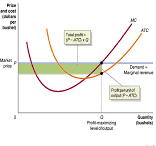

- So How Do Firms Maximize Profit?

- Figuring out how much of a

product should be

produced

- Profit=TR-TC

- To maximize profits the firm

should produce the quantity

where the difference

between total revenue and

total cost is as large as

possible

- MR=(ΔTR)/(ΔQ)

- MR=(Change in total revenue)/(Change

in Quantity)

- MR=(Change in total revenue)/(Change

in Quantity)

- Total Profit= (p-ATC) x Q

- P>ATC, firm has

profit

- P=ATC,

breaks even

- P<ATC, firm

faces loses

- P>ATC, firm has

profit

- MR=(ΔTR)/(ΔQ)

- Profit=TR-TC

- What if the firm is

experiencing loses?

- Long-run decision

- Exit the Market

- Exit the Market

- Short-run decision

- Temporarily stop production

- If, Total Revenue < Variable Cost

- If, Total Revenue < Variable Cost

- Face Sunk Cost

- A fixed cost that is

unavoidable and

can't be recovered

- A fixed cost that is

unavoidable and

can't be recovered

- Continue to Produce

- If, Total Revenue >= Variable Cost

- If, Total Revenue >= Variable Cost

- Short-run supply curve

- Where MC and AVC

meet is the

shutdown point

- MC is the

supply curve

for firms in

SR

- P is the minimum price

where the firm can

continue to produce

- Where MC and AVC

meet is the

shutdown point

- Temporarily stop production

- Long-run decision

- Figuring out how much of a

product should be

produced

- Many Firms

- Firms are Restrained from raising its price because consumers will find another competitor in the market with lower prices

- Horizontal Demand Curve

- Because firms are selling the same

products they can sell as much as they

wants at that times current market

price but won't be able to if the price is

raised

- No matter the quantity sold by a

firm, no effect on the market

price will take place

- Because firms are selling the same

products they can sell as much as they

wants at that times current market

price but won't be able to if the price is

raised

- Resources used

- https://www.quora.com/What-is-a-horizontal-demand-curve-What-are-its-functions

- https://economics.stackexchange.com/questions/13037/is-the-marginal-cost-the-same-for-every-firm-in-a-perfectly-competitive-market

- https://slideplayer.com/slide/12635741/

- http://www.swlearning.com/economics/landsburg/landsburg5e/powerpoint/Ch07/sld004.htm

- http://www.swlearning.com/economics/landsburg/landsburg5e/powerpoint/Ch07/sld004.htm

- https://slideplayer.com/slide/12635741/

- https://economics.stackexchange.com/questions/13037/is-the-marginal-cost-the-same-for-every-firm-in-a-perfectly-competitive-market

- https://www.quora.com/What-is-a-horizontal-demand-curve-What-are-its-functions

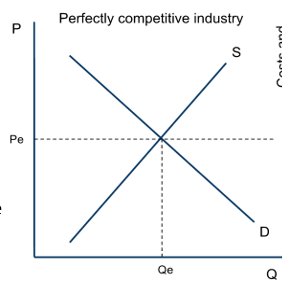

- Prefect Competition Market

- Where

supply

and

demand

lines

meet is

the

equilibrium

- Where

supply

and

demand

lines

meet is

the

equilibrium

Media attachments

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.