300118

Description

Mind Map by Harshad Karia, updated more than 1 year ago

|

|

Created by Harshad Karia

over 12 years ago

|

|

Cash Flow Statements

- Function of the Cash Flow Statements

- Required to be included as part of a company's financial

statements

- A Cash Flow Statement uses information from the accounting records (including income

statements and balance sheets) to show an overall view of money flowing in and out of a

business during an accounting period

- This statement explains to the shareholders why, after a profitable year,

there is a reduced balance at the bank or a larger bank overdraft at the

year end than it was at the beginning of the year

- Required to be included as part of a company's financial

statements

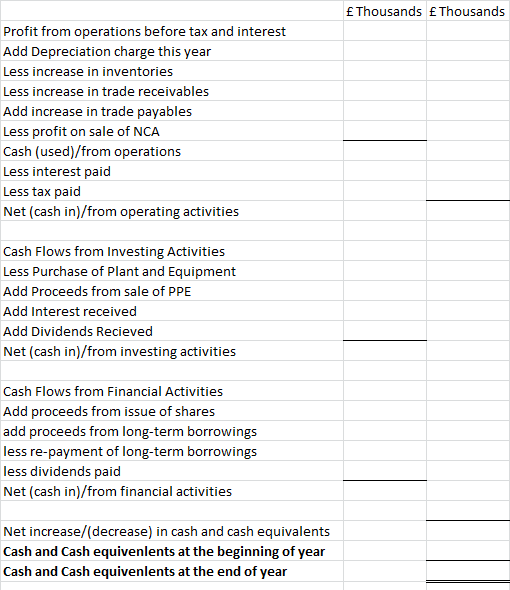

- Format of the Cash Flow Statement

- Operating Activities - the main revenue-producing activities of the business, together with the payment of interest and tax

- Investing Activities - the acquisition and disposal of long-term assets, and other investments

- Financial Activities - Receipts from the issue of new shares, payments to repay shares, changes in long-term borrowings, and dividends paid

- Operating Activities - the main revenue-producing activities of the business, together with the payment of interest and tax

- Gain or Loss on Disposal of Non-Current Assets

- The accounting solution is to transfer any small gain or loss on sale - non cash items - to the income statement

- Have to be careful here as one value will enter in the profits on

the sale of non-current assets and another on proceeds from sale

of non-current assets

- The accounting solution is to transfer any small gain or loss on sale - non cash items - to the income statement

- Revaluation of Non-Current

Assets

- When a revaluation increases the value of an asset, the value of the asset is increased and the amount is placed to a

revaluation reserve in the equity section of the balance sheet where it increases the value of the shareholders' investment in

the company

- This a non cash item so there is no entry in the cash flow

statement

- When a revaluation increases the value of an asset, the value of the asset is increased and the amount is placed to a

revaluation reserve in the equity section of the balance sheet where it increases the value of the shareholders' investment in

the company

- Assessing Cash Flow Statements

- Uses the money measurement concept. only items which can be recorded in money terms can be

included; also we must be aware of the effect of inflation if comparing one year to the next

- Look for positive cash flows from operating activities section. Look at the subtotal 'cash (used in)/from

operations' - this shows the cash from revenue-producing activities before the payment of interest and tax

- Make a comparison between the amount of profit and the amount of cash generated from operations. Identify the major reasons for major differences

between these figures - look at the changes in the net current asset items of inventories, trade receivables and trade payables, and put them into context

- Look at the figures for 'net cash (used in)/from operating activities', ie the cash from operations after interest and tax have been paid. if its

a positive figure, it shows the company has been able to meet its interest and tax obligations to loan providers and tax authorities

- The investing activities section of the statement shows the amount of investment made during the year (E.g. the purchase of non-current assets). In general there should be a

link between the cost of the investment and an increase in loans and/or share capital - it isn't usual to finance non-current assets from short-term sources, such as a bank overdraft

- In the Financing activities section of the statements, where there has been an increase in loans and/or share capital, look to see

how the money has been used. Was it to buy non-current assets, or to finance inventory and trade receivables, or other purposes?

- Look at the amount of dividends paid - this is an outflow of cash that will directly affect the change in the bank balance. As a quick test, the amount of net cash from

operating activities should, in theory, be sufficient to cover dividends paid; if it doesn't , then it is likely that the level of dividends will have to be reduced in future years

- The Cash FLow Statement, as a whole, links profit with changes in cash. Both of these are inportant: without profits the

company cannot generate cash (unless it sells non-current assets), and without cash it cannot pay bills as they fall due

- Uses the money measurement concept. only items which can be recorded in money terms can be

included; also we must be aware of the effect of inflation if comparing one year to the next

- Users of Cash Flow Statements and Why they are interested?

- Shareholders

- • Demonstrates the ability of the company to generate cash from operating activities • Shoes the liquidity of

the business • Identifies the sources of cash and shows how they have been used over the year • Shows

the investment of the company in non-current assets, which should flow through into increasing profits and

share price • Shows the amount of dividends paid to shareholders

- • Demonstrates the ability of the company to generate cash from operating activities • Shoes the liquidity of

the business • Identifies the sources of cash and shows how they have been used over the year • Shows

the investment of the company in non-current assets, which should flow through into increasing profits and

share price • Shows the amount of dividends paid to shareholders

- Loan stock holders/debenture holders

- • Shows the cash available at the year end, thus demonstrates the security of loan stock and debentures

• The financial activities section shows additional loans raised, or repayment of lending • Interest paid to

lenders, in the operating activities section

- • Shows the cash available at the year end, thus demonstrates the security of loan stock and debentures

• The financial activities section shows additional loans raised, or repayment of lending • Interest paid to

lenders, in the operating activities section

- Creditors (Trade Payables)

- • Shows the liquidity of the company and, therefore, the likelihood of being paid for the goods or service

they have supplied • Shows the cash available at the year end for future development which should lead to

suppliers doing more business with the company • Shows whether the company is financing itself through

lending (which usually repaid ahead of trade payables in the event of the company ‘going bust’) or through

shareholders (which rank after trade payables) • Shows flows of cash, it is considered to be the most

objective of the three main financial statements – thus it gives a good picture of the state of the company’s

finances

- • Shows the liquidity of the company and, therefore, the likelihood of being paid for the goods or service

they have supplied • Shows the cash available at the year end for future development which should lead to

suppliers doing more business with the company • Shows whether the company is financing itself through

lending (which usually repaid ahead of trade payables in the event of the company ‘going bust’) or through

shareholders (which rank after trade payables) • Shows flows of cash, it is considered to be the most

objective of the three main financial statements – thus it gives a good picture of the state of the company’s

finances

- Managers and Employees

- • Highlights further information on the state of the company’s finances that is not readily available from the

income statement and balance sheet • Identifies the sources of cash and shows how they have been used

over the year • Shows the cash available at the year end for future development of the company and,

therefore, security of employment • May help managers with decision-making and development of the

company • A surplus of cash for the year may indicate to employees that the company can afford pay

increases

- • Highlights further information on the state of the company’s finances that is not readily available from the

income statement and balance sheet • Identifies the sources of cash and shows how they have been used

over the year • Shows the cash available at the year end for future development of the company and,

therefore, security of employment • May help managers with decision-making and development of the

company • A surplus of cash for the year may indicate to employees that the company can afford pay

increases

- Other users – potential investors, stock market analysts, the bank, customers and the public

- Shareholders

- Layout

Media attachments

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.