458149

The Determination of

Equilibrium Market Prices

- EQUILIBRIUM=

the price at

which demand

is equal to

supply and

there is no

tendency for

change

- DISEQUILIBRIUM= a situation within the market where supply does not equal demand.

- EXCESS SUPPLY= when supply at a particular price is greater

than demand; this should signal to producers to lower prices

- EXCESS DEMAND= when demand is greater than supply at a given price

- MARKET-CLEARING PRICE= the price at which all goods that are supplied will be demanded

- Excess Supply and Excess Demand

- The effect of a TAX

- always affects SUPPLY

- price rise to the consumer is P1P2

- the tax is the vertical distance between

the two supply curves so is greater

than the price rise to the consumers

- the tax is the vertical distance between

the two supply curves so is greater

than the price rise to the consumers

- P2= Ptax

- price rise to the consumer is P1P2

- always affects SUPPLY

- The effect of a SUBSIDY

- always affects SUPPLY

- price rise to the consumer is P1P2

- the subsidy is the vertical

distance between the two

supply curves (P1P3)

- the subsidy is the vertical

distance between the two

supply curves (P1P3)

- P2= Psub

- always affects SUPPLY

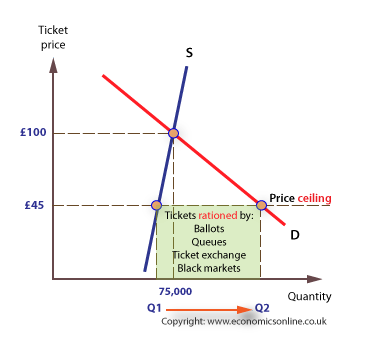

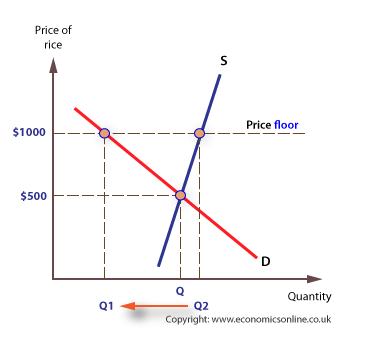

- PRICE CEILINGS AND PRICE FLOORS

- Maximum prices (price ceilings)

- has to be set

below equilibrium

to have an effect

- there will be excess

demand as the price is

low, this can be dealt

with through queues,

waiting lists etc but

may result in a black

market emerging

- has to be set

below equilibrium

to have an effect

- Minimum prices (price floors)

- has to be set above equilibrium (free market price) to have an effect

- e.g. minimum wage, designed to increase

standards of living for low paid workers

- has to be set above equilibrium (free market price) to have an effect

- can distort the signals within the market as they're imposed by the

government and are not natural, leading to a misallocation of resources

- Maximum prices (price ceilings)

Media attachments

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.