Page 1

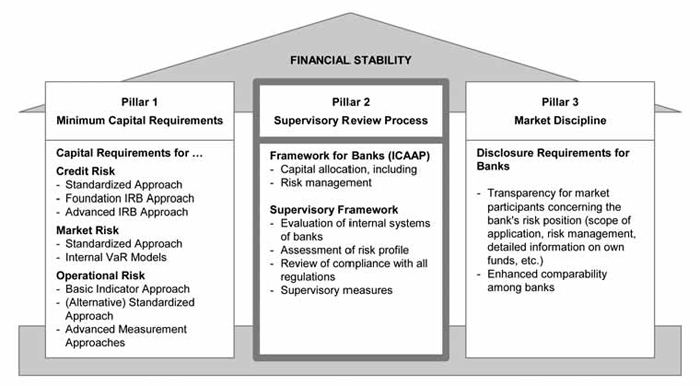

Basel II Three Pillars Approach: In response to the criticism of Basel I and its amendment, a number of changes were made More option for banks to determine its capital charge for risk improved credit risk weighting Recognition of operational risk Subject to National supervisory approval, banks will be allowed to use their own internal rating models as a measurement of risk Introduction of "Supervisory" and "Market Disciple" pillars

{kind=link}

The fundamental ratio to be computed in Basel II for the minimum capital requirements is: Capital (tier 1 and 2) / Amended credit risk + market risk + operational risk

Criticism of Basel II: The internal approach to forecasting risk, based on VaR, neglects crucial aspects of risk in the financial markets. It is assumed that the bank’s own actions, based on its forecast of future volatility, does not affect this volatility. Financial risk is created by the market behavior of all agents, including the banks which are forecasting their risk. This leads to the contagion phenomena known from financial crises, where expectation of falling prices triggers more sales with an increased down- turn of prices as result Too many rules, excessive prescription Pro-Cylclical - A condition where value of goods and services tend to move in correlation with the economy Failure to recognise benefits of diversification. Overestimating risk of lending to developing countries. High cost of implementation

The main points of Basel III: Increased capital reserves: In addition to the existing system of capital regulation, two new Items are added, namelycapital buffer, which comes into force in cases where the activities of the bank increase very rapidlycountercyclical buffer, which should prevent the tendency that capital reserves according to the existing rules will be small during booms and large in slumps Leverage rule: This is a rule which is aimed to prevent too small capital reserves even in cases where assets have low risk and therefore would not give rise to building up reserves by using the existing rules Liquidity rules: High quality assets should be large enough to cover one month net cash out- flow.

The Financial Services and Markets Act was passed in 2000. It established the FSA as the sole regulator of all UK financial institutions.

FSA Goals: Maintain confidence in the UK financial system Educate the public with risk associated with different forms of investing Protect consumers but encourage them to take responsibility for their financial decisions Reduce financial crime

FSA Risk Based Approach To Regulation:The core of the operating framework for the FSA is sometimes described by the acronym, ARROW, which stands for Advanced, Risk-Responsive Operating Framework. ARROW defines the essence of the FSA's risk-based approach to regulating financial markets, services, and firms. As supervisor for all financial institutions, the FSA is trying to move away from specific rules for each of the different types of financial institutions The RTO Approach (risk to our objectives) involves computing a score for each firm supervised by the FSA. The score shows the probability of the firm having an impact on the ability of the FSA to meet its statutory objectives The score is obtained from a simple equation: Impact Score = Impact of the problem X Probability of the problem arisingA firm’s score determine how closely the FSA monitors it

The FSA (Financial Services Authority) is an independent, non-governmental body that regulates the financial services industry in the UK, including most financial services markets, exchanges and firms. It sets standards to which such organizations must comply and can take action against them should they fail to meet required standards.

Bank structure and regulation in the USA: Large number of banks, banking market not concentrated Federal Reserve System: 12 Federal Reserve Banks By the 1990s, 92% of banks were owned by BHCs (any firm holding at least 25% of the voting stock of a bank subsidiary); BHCs could circumvent the interstate branching laws, via “multi-bank” holding companies

The US Financial Holding Companies: Supervision of the FHCs is functional, i.e. insurance firms continue to be supervised by the Department of Trade and Industry, investment banks by the Securities and Exchange Commission, and the banking subsidiaries by the Federal Reserve Bank Firewall between commercial securities subsidiaries: they are prohibited from cross marketing with each other, and a bank can sell but may not underwrite insurance

US Branch Banking Regulations: To discourage concentration in banking sector there were limitation in setting up banks’ branches, mainly interstate branching Each state had different degrees of restriction Bank Holding Companies might establish bank subsidiaries in each state, but each was an individual legal entity, which had to be separately capitalised In 1994 the Riegle Neal Interstate Banking and Branching Efficiency Act largely eliminated these restrictions To prevent excessive concentration, a BHC/FHC may not hold more than 30% of total deposits in any given state, and 10% nationally

Deposit Insurance in US: All member banks of the Federal Reserve System are required to join the Federal Deposit Insurance Corporation (FDIC) The FDIC member banks pay an insurance premium, which is used to purchase securities to provide the insurance fund with a steam of revenue The FDIC insures deposits of up to $ 100,000; deposits are fully insuranced and it can creates moral hazard problems Premia are linked to capital at risk

Bank Structure in Japan: Keiretsu system A Keiretsu is a group of companies with cross-shareholdings and shared directorships which normally include a bank, trust company, insurance firm and a major industrial concern (i.e. cars, steel) The bank supplies services to the other keiretsu members, including loans The Ministry of Finance (MoF) was the key regulator through three bureaux: Banking, Securities and International Finance

Bank Regulation in Japan: MoF’s responsibilities included all aspects of financial institution supervision: examination of financial firms, control of interest rates and products, supervision of the deposit protection scheme, setting the rules on activities to be undertaken by financial firms Bank of Japan was responsible for the implementation of monetary policy, but under the influence of MoF High protected market Japanese companies largely dependant on banks’ loans

Theories (Functions) for Financial Intermediation: Delegated Monitoring Information Production Liquidity Transformation Consumption smoothing Commitment Mechanisms

Basel II & III

Bank Structure and Regulation

General

Want to create your own Notes for free with GoConqr? Learn more.