14268129

Description

Flashcards by Carley O'Connor, updated more than 1 year ago

|

|

Created by Carley O'Connor

almost 6 years ago

|

|

| Question | Answer |

| THE FINANCIAL SYSTEM | Umbrella term covering: 1) Financial Markets 2) Financial Institutions 3) Financial Assets & Liabilities |

| Financial Markets | Divided into different types: - Capital Markets (Stock-markets) - Money Markets (debt finance & investment) - Commodity Markets (trading e.g. oil/metal/agriculture) - Derivatives Markets (instruments for management of financial risk e.g. options and futures contracts) - Insurance Markets (redistribution of risks) - Foreign Exchange Markets (trading of foreign exchange) |

| Stock Market | Acts as a market for: -Shares in publicly quoted LLCs -New share issues by these companies -gov't stocks & bonds Prices are determined by demand and supply. (Demand reflects investors' estimates of the prospects for the company) Demand for shares also reflects yields (yields on bonds are determined by their price & interest rate) Stock Markets provide long term finance & are part of the capital market |

| Money Markets | Acts as a market for treasury bills, commercial bills, CDs and other short term debt Stock market (Capital market): maturities > 1 year Money Market: maturities < 1 year |

| Financial Intermediaries | Roles: Risk reduction Aggregation Maturity transformation Financial intermediaries (Can be deposit taking institutions such as banks and building societies or non-deposit-taking institutions such as insurance companies, pension funds and investment trusts.) |

| Risk Reduction | By lending to a wide variety of individuals and businesses, financial intermediaries reduce the risk of a single default resulting in total loss of assets |

| Aggregation | By pooling many small deposits, financial intermediaries are able to make much larger advances than would be possible for most individuals |

| Maturity Transformation | Most borrowers wish to borrow in the long-term whilst most savers are unwilling to lock up their money for the long-term. Financial intermediaries, by developing a floating pool of deposits, are able to satisfy both the needs of the lenders & borrowers |

| Financial Intermediation | Financial intermediaries bring together lenders and borrowers through a process known as financial intermediation |

| Most lenders wish to offer their funds for the short term whereas most borrowers want to borrow over the longer term. Resolving this mismatch is known as: A) Risk reduction B) Aggregation C) Maturity Transformation D) Pooling | C) Maturity Transformation The time period money is lent/borrowed is called the maturity |

| Working Capital | Funds to finance day-to-day business including payments for wages and salaries, raw materials & components short-term instruments should be chosen to finance the short-term needs |

| Investment Capital | Funds to finance the purchase of new capital equipment or to finance acquisitions & mergers long-term instruments should be chosen to finance the long-term needs |

| Asset Management Function | Suitable instruments for investing any surplus funds |

| Sources of Finance: Long-term | - Internally generated funds (retained profits) - Equity generated by the issuing of additional shares in the company - Debt finance by borrowing funds from financial insitutions ( |

| Sources of Finance: Short-term | For organisations & individuals= financial needs can be met by the banking system & money markets - They deal in short-term financial instruments: cash current accts overdrafts & short-term loans CDs bills of exchange trade credit Main providers: commercial banks finance houses other companies |

| Surpluses & Deficits Financial Needs: Organisations | (arising from non-synchronisation of payments & receipts) - Short-term: need for working capital to finance production - Medium-term: arising from costs & payments in longer term contracts & production processes - Long-term: arise from financing investment projects |

| Surpluses & Deficits Financial Needs: Individuals | Individuals have liquidity surpluses & deficits - Short run: income normally arrives monthly but expenditure is continuous - Medium-term: expenditure has peaks, e.g. christmas & holiday, and lows other times of the year. Also purchase of consumer durables, e.g. cars, raises medium-term liquidity problems - Long-term: especially for purchases of houses. |

| Surpluses & Deficits Financial Needs: Goverments | Governments current expenditure is steady over the year, but tax revenue is not, hence short run liquidity shortages & surpluses. Governments undertake longer term projects including public investment which have to be financed in the longer term In the the long run, government must manage the national debt. This is the accumulated government debt resulting from previous borrowing. |

| Mezzanine Finance | Combines aspects of both debt and equity finance. Although the finance is initially given as a loan (debt capital), the lender has the rights to convert to an equity interest in the company if the loan is not paid back in time and in full. |

| ABC Chocolate manufactures a range of different chocolate novelties for sale in major supermarkets. It has seasonal trade and finds the period before Christmas difficult from a cash management point of view as it has to pay out wages and for ingredients before the holiday period but often has to wait until the New Year before receiving payment from major customers. Which of the following would be a suitable way of managing this cash flow problem? A) Issue new equity shares B) Overdraft C) Leasing arrangement D) Mortgage | B) Overdraft The easiest way to see this is to consider the timescales involved. The shortfall is short term and relates to the lack of synchronisation between receipts & payments |

| In recent years FGH, a high-end furniture retailer, has appeared to favour mezzanine finance to alternative forms of finance. What is meant by the term 'mezzanine finance'? A) Short-term loans to help a firm through cash flow crisis B) Foreign currency loans C) Loans by non-financial institutions D) Finance that is neither pure debt nor pure equity | D) Finance that is neither pure debt nor pure equity Mezzanine finance is a type of 'middle ground' finance which has characteristics of both debt & equity |

| Financial products: EQUITY (ordinary shares) | Companies often raise funds through the issue of shares. Ownership of companies is conveyed via ordinary shares. CHARACTERISTICS: Returns- potential for high returns if company is profitable Risk- shares carry high risk. Profit falls= danger of 0-low dividends & low share value Timescales- usually no intention of buying back shares, so equity is long-term Liquitdity- quoted companies=highly liquid & investors can cash in at any point unquoted= very difficult to sell shares |

| Financial products: BONDS | CHARACTERISTICS: Return- low returns because lower risk Risk- lower risk than equity. Bonds may be secured and interest rate fixed Timescales- maturity is defined on the bond and varies form short term (treasury bills) to long term (25 year corporate bonds). Some bonds are redeemable and some not Liquidity- Unquoted= investor has no choice but to wait for redemption. Quoted= easier to liquidate by selling on bond markets |

| Financial products: CDs (Cert. of Deposit) | CHARACTERISTICS: Returns- very low due to low risk Risk- very safe Timescales- 3 & 6 month maturities are most common Liquidity- can be readily sold on money markets |

| Financial products: Credit Agreements | CHARACTERISTICS: Returns- usually high interest rates Risk- credit card company faces risk of default Timescales- usually short term, some get into financial difficulty by running up large debts they can't repay Liquidity- debt can't be resold to lender, but borrower may be able to repay early |

| Financial products: Mortgages | CHARACTERISTICS: Return- low as it will be secured on property bought Risk- low. A fall in house prices would reduce value of security offered Timescales- Long term (10-35 years) Liquidity- traditionally can't be resold by the lender to recover their funds |

| Financial products: Bills of Exchange | (contract between 2 traders, the buyer promising to pay a sum of $ in return for goods) CHARACTERISTICS: Return- difference between buy/sell price & redemption value Risk- may be guaranteed by banks Timescales- short-term (3-6 months) Liquidity- can be resold on money markets |

| TUL have surplus funds that they wish to invest. Which of the following would be the least risky investment? A) Certificates of Deposit form a global bank B) Equity shares in a new growing company C) Unsecured loan stock D) National lottery tickets | A) Certificates of Deposit form a global bank Risk looks at the degree of uncertainty of future cash flows. The CD will be the least risky out of the options given. |

| Yields on Bonds | 3 Ways to calculate: 1) the bill rate- AKA coupon rate 2) Running yield (running rate or interest yield)- =(annual interest / market value) X 100% (note: annual interest is bill rate) 3) Gross redemption yield= gives the annualised overall return to the investor & incorporates both interest & capital gains & losses (note: calculation is outside of syllabus) |

| Yields on Equity | Dividend Yield= dividend per ordinary share --------------------------------- X 100% market price of the share (example= company pays 30 cents with market price of $7.50. 30 cents ------------- X 100% = 4% 750 cents |

| Pumpkin has $100 stock with a market price of $80 and a dividend of $5. It will generate a yield of: A) 5% B) 8% C) 6.25% D) 12.5% | dividend= $5 market price= $80 5/80= 0.0625 x 100%= 6.25 C) 6.25% |

| Suppose a company wants to issue some bonds and is concerned about the level of return it will receive. Which of the following yields does not need knowledge of a bond's market value to calculate it? A) Running yield B) Gross redemption yield C) Bill rate D) Interest yield | C) Bill rate This is the same as the coupon rate. |

| Central Rate of Interest | Rate the central bank would lend to the money market. A "base" rate if you will |

| Real and Nominal Interest Rates | Real- Puts interest rates in the context of inflation. It shows interest rate, allowing for inflation. Suppose inflation is 3% and you deposit $100 paying 4% annum. Nominal rate is 4% & end up with $104 3% of the increase covers inflation, so your wealth is only increased by 1% Nominal equation (not expected to do) 1+r=(1+m)/(1+i) r=real rate m=money rate i=level of inflation (drop off the 1 when get the answer) |

| AUSL is considering an investment within the year. They are concerned about interest rate volatility. Which of the following are the likely consequences of a fall in interest rates? (i) A rise in the demand for consumer goods. (ii) A fall in investment. (iii) A fall in government spending. (iv) A rise in the demand for housing. A) (i) and (ii) only B) (i), (ii) and (iii) only C) (i), (iii) and (iv) only D) (ii), (iii) and (iv) only | C) (i), (iii) and (iv) only A fall in interest rates will encourage investment, not a fall in investment. Lower interest rates reduce gov't expenditure on servicing the national debt, & will encourage consumers to take on more credit, including borrowing for house purchase. |

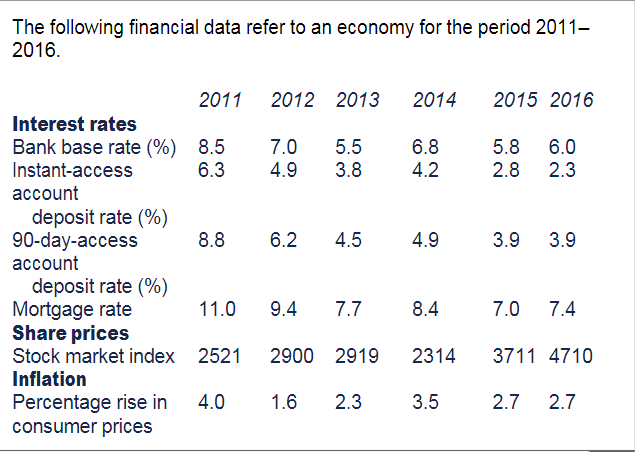

| (i) Using the bank base rate, calculate the real rate of interest for 2013. (ii) Calculate the real mortgage rate of interest for 2014. (iii) State whether real share prices rose or fell between 2012 & 2013. | (i) Bank base rate= 5.5% Inflation rate= 2.3% 1.055/1.023 x 100% - 1= 3.1% (ii) Mortgage rate= 8.4% Inflation rate= 3.5% 1.084/1.035 -1 x 100%= 4.7% (iii) The share price index represents the change in money values. % increase in share index 2012-2013= (2919-2900)/2900= 0.66% Inflation of the same period= 2.3% As share prices have grown at a lower rate than inflation then in real terms the prices have fallen. |

| True or False. Rising real interest rates will encourage savings and investment. | False- high interest rates encourage savings but discourage biz investment |

| True or False. Interest rates will only affect business investment if that investment is financed by borrowing. | False- A rise in interest rates raises the opportunity cost of using internal funds to finance investment |

| True or False. Rising interest rates in a country tend to raise the exchange rate for that country’s currency. | True- Higher interest rates encourage capital inflows which increase the demand for the currency |

| True or False. Producers of consumer durable goods are more sensitive to changes in interest rates than supermarkets. | True- Consumer durables are often bought on credit |

| True or False. Central banks cannot increase the money supply and raise interest rates at the same time. | True- If the supply of money increases, its price, the rate of interest, will go down. |

| State whether the effect of a rise in interest rates will be to: Increase or Decrease gov't spending | Increase The cost of financing gov't debt would increase |

| State whether the effect of a rise in interest rates will be to: Reflate or Deflate the economy | Deflate It would discourage expenditure |

| Which one of the following is not a function of a central bank, for example the Bank of Japan? A) Management of the National Debt B) Holder of the foreign exchange reserves C) The conduct of fiscal policy D) Lender of the last resort | C) The conduct of fiscal policy Fiscal policy is concerned with the government budget and the balance of taxation and public expenditure. This is the responsibility of the government, not the central bank. |

| What is Cash ratio? | The amount of cash kept by banks in readiness to pay withdrawals as a proportion of their total assets. |

| What is the relationship between liquidity & profitability of banks assets? | The most liquid assets, for example cash, are the least profitable; and the least liquid assets, for example advances & loans to customers, are the most profitable |

| How could a central bank reduce the supply of credit in the financial system? | The central bank would need to reduce the liquidity of the financial system as this is the basis upon which credit is created. It can do this by selling government stocks to financial institutions. |

| How could a central bank reduce the demand for credit in the financial system? | The central bank could raise interest rates as interest is the price of credit and a higher price will reduce demand. |

| What are capital adequacy rules? | Capital adequacy rules attempt to ensure that banks have sufficient capital to cover potential bad debts on risk assets. |

| Which of the following would be expected to lead to a rise in share prices on the Hong Kong stock exchange? A) A fall in interest rates B) A rise in the rate of inflation C) A fall in share prices in other stock markets D) An expected fall in company profits | A) A fall in interest rates A fall in company profits would clearly discourage the purchase of shares and so share prices would fall. Since stock markets are linked, a fall in one market tends to lead to a fall in share prices in other markets. A rise in inflation would lead to some business pessimism and might be expected to lead to a rise in interest rates. However, since share prices and interest rates move in opposite directions, A is the correct solution. |

| A 30 year Treasury bond that was issued last year is sold in a: (i) money market (ii) capital market (iii) primary market (iv) secondary market A) Both (i) and (iii) B) Both (i) and (iv) C) Both (ii) and (iii) D) Both (ii) and (iv) | D) Both (ii) and (iv) The bond can be sold in a capital market and a secondary market |

| The function of linking net savers and net borrowers is: A) known as the credit multiplier B) one of the functions of money C) solely the function of the capital market D) called the financial intermediation | D) called the financial intermediation |

| A bond with a nominal value of $1,000 has coupon rate of interest of 6% and market value of $1,200. Calculate the yield on this bond. | (annual interest / market value) x 100% bond nominal value= $1,000 interest rate= 6% annual interest= $60 $60 / $1,200 x 100%= 5% |

{kind=link}

Want to create your own Flashcards for free with GoConqr? Learn more.