8100315

Description

Mind Map by Harry Lewis, updated more than 1 year ago

|

|

Created by Harry Lewis

about 7 years ago

|

|

Labour, capital, investment and capacity

- Investment

- Definition - any form of

capital intended to

contribute to future output

- Can be physical - land premises,

and equipment - or human

capital such as training and

education

- Investment increases

productivity->revenue and

spending power raised->more

investment

- Wages increase, which

encourages

labour-saving investment

- Technological changes

make investment

cheaper

- Increasing capital entails net

investment - additions of

extra equipment rather than

just replacements

- Level of profit depends on level of investment; but

some large corporations with abnormal profits may

not reinvest

- Level of profit depends on level of investment; but

some large corporations with abnormal profits may

not reinvest

- Standards of living raise over time as

capital becomes relatively cheaper

as wealth increases

- It becomes worthwhile to equip workers with

more equipment rather than use more

workers - more capital intensive production

- New technologies may only be

affordable to the biggest businesses

- Case for antitrust rules to spread the

availability of technology?

- Case for antitrust rules to spread the

availability of technology?

- Definition - any form of

capital intended to

contribute to future output

- Labour intensive process

- Some occupations remain labour

intensive because of the nature of

the work, mostly services such as

medical care and hairdressing

- These tend to be small firms in more monopolistic

markets, as labour intensive production will

typically be on quite a small scale

- These tend to be small firms in more monopolistic

markets, as labour intensive production will

typically be on quite a small scale

- Some occupations remain labour

intensive because of demand for

craftsmanship and artistic flair - these

small niche businesses may thrive

alongside the larger ones

- Developing countries have little capital equipment, but

labour is cheap. People have no disposable income to

spend on capital, so employers keep these costs to a

minimum and employ more people.

- Some occupations remain labour

intensive because of the nature of

the work, mostly services such as

medical care and hairdressing

- Market change

- Much capital is purpose-designed, meaning that

when there are changes in demand it may be

difficult for capital-intensive businesses to adapt

- They can get around this by ensuring their

equipment is flexible, for example using

computer aided manufacturing

- This, however, might increase overall costs

- This, however, might increase overall costs

- They can get around this by ensuring their

equipment is flexible, for example using

computer aided manufacturing

- Labour intensive production is more

flexible, as skills can be adapted easily.

However, if markets shift away from

products entirely, jobs are lost.

- Much capital is purpose-designed, meaning that

when there are changes in demand it may be

difficult for capital-intensive businesses to adapt

- Technological change

- New technologies can facilitate capital

intensive mass production, for

example computers, which used to be

a niche market but are now mass

produced for all

- New technologies introduced -> new processes use more capital -> productivity rises -> costs fall -> prices fall -> sales increase -> new jobs are created

- Changing market structures

- New technologies introduced -> new processes use more capital -> productivity rises -> costs fall -> prices fall -> sales increase -> new jobs are created

- New technologies can facilitate capital

intensive mass production, for

example computers, which used to be

a niche market but are now mass

produced for all

- Capacity utilisation

- Investment and technological change

increase the capacity of business and the

economy

- How is investment performed? R&D through

government or companies themselves?

- How is investment performed? R&D through

government or companies themselves?

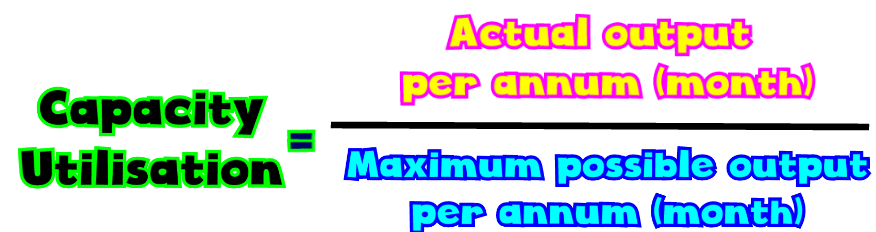

- Capacity utilisation measures

how much of the maximum

possible output is actually

produced.

- If capacity is fully

utilised, costs will be

minimised but it may be

difficult to respond to

increases in demand.

- However, if slack is kept in the

system average costs may rise

which might be a problem in a

highly competitive market

- If demand is insufficient, there will be

under-utilised capacity. This means that

fixed costs are shared across a lower level

of output and therefore average fixed

costs will rise

- A business may try to increase its productivity in this scenario by

diversifying or using aggressive market strategies. If demand

seems stuck below capacity, capacity will have to be cut.

- Link to marketing strategies

- Link to marketing strategies

- High levels of unemployment suggest that the

economy as a whole is working below capacity.

- Although not exactly the same as allocative efficiency,

this idea can be used in conjunction with it

- Although not exactly the same as allocative efficiency,

this idea can be used in conjunction with it

- A business may try to increase its productivity in this scenario by

diversifying or using aggressive market strategies. If demand

seems stuck below capacity, capacity will have to be cut.

- However, if slack is kept in the

system average costs may rise

which might be a problem in a

highly competitive market

- Investment and technological change

increase the capacity of business and the

economy

- Efficiency

- Efficiency is achieved when best possible

use is made of all the resources employed in

production.

- Similar to allocative efficiency

- Similar to allocative efficiency

- Efficient organisation of production processes

should contribute to increase output per hour

worked.

- Ultimately, higher productivity allows businesses to cut

costs, reduce prices and become more competitive.

- However, will cutting costs always be

the best pricing strategy?

- However, will cutting costs always be

the best pricing strategy?

- Efficiency is achieved when best possible

use is made of all the resources employed in

production.

Media attachments

{kind=link}

Want to create your own Mind Maps for free with GoConqr? Learn more.